Markets absorbed the large supply of euro area sovereign bonds well as yields rose to meet investor expectations. Investor demand for Finnish government bonds remained solid.

In 2025, the Republic of Finland successfully carried out EUR 47.3 billion of debt issuance. Net borrowing amounted to EUR 17.8 billion. At the end of 2025, Finland’s central government debt totaled EUR 187.7 billion, or 66.7% relative to GDP (61.2% in 2024).

In 2025, the Republic of Finland successfully carried out EUR 47.3 billion of debt issuance. Net borrowing amounted to EUR 17.8 billion. At the end of 2025, Finland’s central government debt totaled EUR 187.7 billion, or 66.7% relative to GDP (61.2% in 2024).

At year-end, the effective cost of central government debt was 1.86% (2.01%), the average fixing of the central government debt 5.4 years (4.9), and the duration 4.2 years (3.9).

These figures are presented in the State Treasury’s Debt Management Annual Review published today, which outlines developments in central government borrowing, cash and risk management, and provides an overview of the operating environment in the government bond market in 2025.

Parliamentary agreement on curbing indebtedness important signal

Although the underlying backdrop for European government bond issuance turned out to be supportive in 2025 – a damaging escalation of global trade war was avoided, and monetary policymakers saw no imminent threat to inflation on either side of the Atlantic– global uncertainties and mounting government expenditure pressures led to steeper yield curves in European government bonds, including Finland’s.

“Rising yields and a steeper curve improved investors’ return prospects, even though Finland’s spread to Germany tightened over the course of the year,” says Anu Sammallahti, Head of Debt Management at the State Treasury.

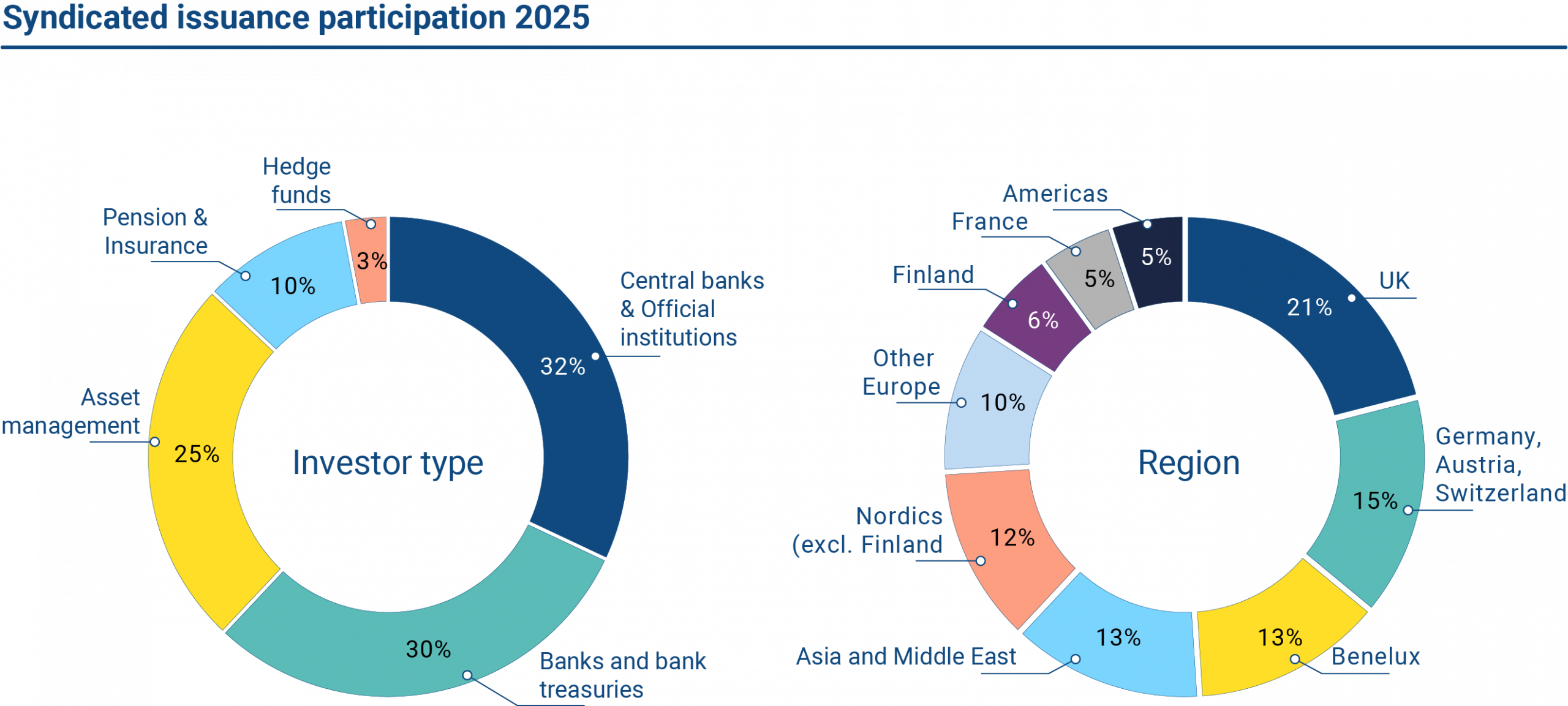

Investor demand for Finnish government bonds remained solid. The syndicated bond issuance of 2025 demonstrated record‑large order books in comparison to recent years.

The investor base for Finnish central government debt is largely

European.

While fixed-income investors assess the economic growth potential of their sovereign bond holdings, they also value prudent fiscal policy. Thus the broad parliamentary agreement on fiscal targets reached in Finland at the end of the year is a key signal of future fiscal policy, Sammallahti concludes.

“The reformed national fiscal framework should be viewed as a signal for constraining indebtedness with a target-oriented fiscal policy extending beyond electoral cycles” she says.

Management of Finland’s public finances touches upon broader structural questions:in addition to debt ratios, topical issues include economic growth prospects, population ageing, and long-term preparedness of society. This is evident, for example, in the ongoing discussion on the Finnish pension system.

Public debt management is by nature a long‑term activity – and the overall state of the public household matters from an investor perspective as well.

“Sizeable pension assets strengthen public finances when the population is aging and that prefunding also supports the issuer profile and investors’ credit risk assessments,” Sammallahti notes.

The 150-year history of State Treasury and government borrowing

The State Treasury began its operations in January 1876 as a new central agency of the Grand Duchy of Finland, responsible for managing state funds and executing interest payments and amortisations on government debt. The Debt Management Annual Review 2025 includes an article on the long and eventful history of government borrowing, extending well beyond 150 years, written by Mika Arola, DSc (Econ.), who has long served in senior debt management roles at the State Treasury.

The development of the Finnish state and its borrowing have gone hand in hand. Finland has been built, industrialised, developed – and during wartime defended – with the help of debt financing. Already in the late 19th century, government borrowing was highly international: by issuing sovereign bonds in the financial centers of the Western world, Finland positioned itself early on as part of the West and built its narrative as an independent state.

EU membership presented a major transformation in government borrowing, as the world’s second-largest bond market became Finland’s domestic market. There was a radical change in the investor base within a few years as international investors replaced domestic pension institutions. In 2025, only a few percent of Finland’s central government debt is held by domestic investors; the core investor base consists of institutional investors in Europe, including the Nordic countries and the United Kingdom.

“Since the days of the autonomous Grand Duchy, the history of borrowing has underscored the importance of creditworthiness. And after joining the euro area, broadening the investor base without foreign exchangerisk was a key change in the operating environment,” Sammallahti sums up.

Read the review: treasuryfinland.fi/annualreview2025

Further information: Anu Sammallahti, Director of Finance, tel. +358 295 50 2575, anu.sammallahti(at)valtiokonttori.fi

Key figures of central government debt management in 2025 (2024):

- Gross borrowing: EUR 47.3 billion (42.8 billion)

- Net borrowing: EUR 17.8 billion (12.6 billion)

- Number of emissions: 69 (83)

- Average yield on Finland’s 10‑year government bond: 3.02% (2.85%)

- Effective cost of central government debt at year-end: 1.86% (2.01%)

- Average fixing of central government debt at year-end: 5.4 years (4.8 years)

- Average maturity of central government debt at year-end: 7.84 years (7.75 years)

- Interest expenses: EUR 3.0 billion (3.2 billion)

- Total secondary market turnover: EUR 155.2 billion (121.3 billion)