The strategic goal of debt management is to ensure the central government’s financing needs are met cost‑effectively under all market conditions while minimising the long‑term cost of debt within an acceptable level of risk.

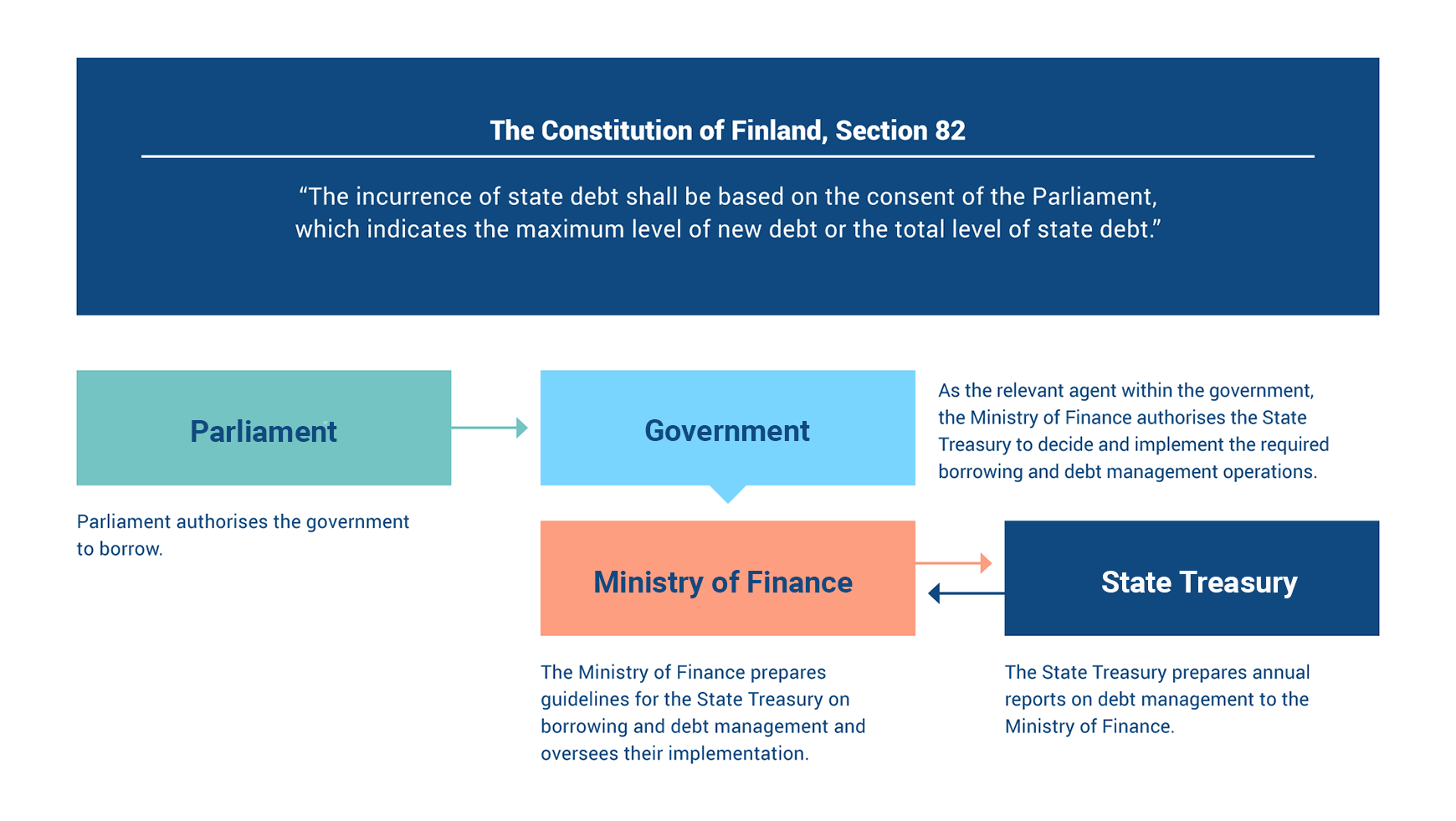

Framework of government borrowing

The strategy for central government debt management is set by the Ministry of Finance. The State Treasury carries out its debt management tasks according to the Ministry’s directive.

The Ministry’s directive sets out the general principles and objectives of debt management, the instruments and risk level, as well as any other applicable restrictions. The State Treasury is authorised to raise funds provided that the nominal value of the central government debt does not exceed EUR 205 billion. Of this amount, up to EUR 35 billion may by short-term debt.

The State Treasury is authorised to take out short-term loans when necessary to safeguard the central government’s liquidity and, as part of its risk management, to enter into derivative agreements that comply with the terms and instructions issued by the Ministry of Finance.

The State Treasury reports regularly to the Ministry of Finance on its debt management. Key information on the central government’s debt management is also published annually in the central government’s financial accounts and the Government’s annual report. The final central government accounts are published every year in March and the Government’s annual report in May.

The infograph shows the legal framework and the division of functions of government borrowing between the Parliament, the Government, the Ministry of Finance, and the State Treasury.

Risk management: an essential part of sound debt management

The goal of risk management is to avoid unexpected losses and safeguard the continuation of operations. The aim of central government is to manage all risks in a systematic manner. Its risk management process consists of identification of risks, quantification and evaluation of risks, risk monitoring and reporting, and active management of its risk positions.

The main risks are financing risk (long-term refinancing risk and short-term liquidity risk), credit risk, market risk (interest and exchange rate risk), operational risk, and legal risk.

Financing risk

Financing risk can be divided into liquidity risk and refinancing risk. Liquidity risk refers to short‑term funding risks, essentially the amount of financing the government must cover in the near term relative to its liquid assets and funding capacity. Refinancing risk measures the volume of debt that needs to be refinanced over a given period, such as within one year.

Liquidity risk is managed by the State Treasury by maintaining a sufficiently large cash buffer at all times. The buffer will be larger if uncertainty related to the availability of funding is perceived to rise. The Ministry of Finance’s debt management directive sets a minimum target period for how long the central government must be able to cover its known and expected expenditures without new borrowing.

Liquidity risk management is based on a cash flow forecast system covering the entire central government sector, through which government accounting entities report their projected income and expenditures to the State Treasury. The State Treasury’s cash management relies on this data to assess the adequacy of the cash buffer. In line with the Ministry of Finance’s directive, the State Treasury safeguards liquidity primarily by investing the cash reserves in the Bank of Finland. Cash reserves can also be invested in other collateralised or low-risk short-term maturities.

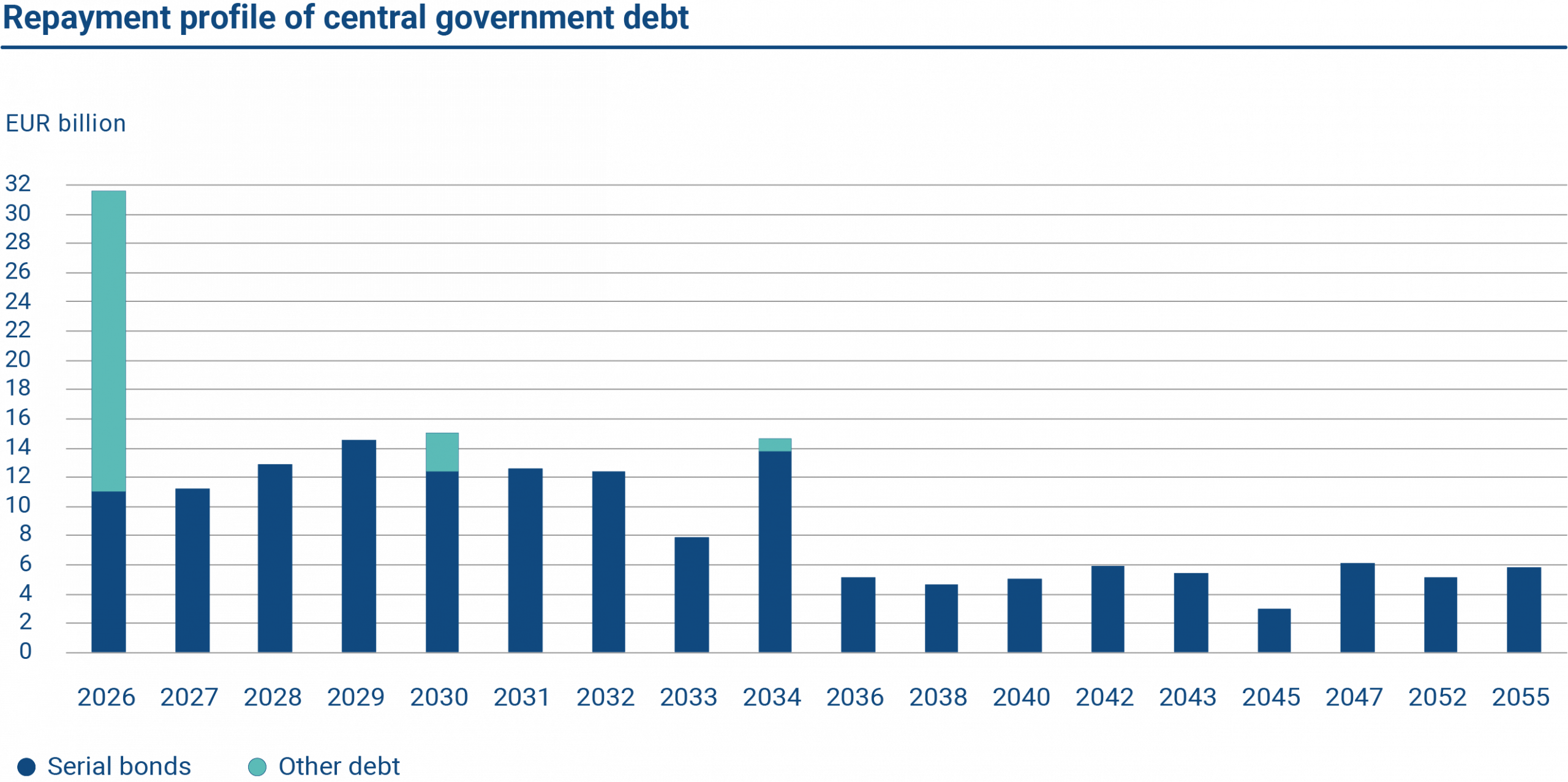

The State Treasury manages refinancing risk first and foremost by avoiding large maturity concentrations of debt. The Ministry of Finance’s debt‑management directive sets limits to this. Refinancing risk is further reduced by diversifying funding across instruments, investor types and geographical regions. This mitigates reliance on any single source of financing and enhances the liquidity and investor appeal of government bonds.

The graph shows the repayment profile of central government debt.

Credit risk

Credit risk arises from the investment of cash assets and derivative agreements. The government requires its counterparties to have a high level creditworthiness, and the Ministry of Finance’s directive sets limits and minimum thresholds for the credit ratings of counterparties. Credit risk management is particularly critical in large cash investments. To reduce the credit risk associated with cash investments, the State Treasury primarily invests cash assets in the Bank of Finland and additionally in, for example, secured tripartite repo agreements.

The State Treasury uses collateral to reduce the long-term credit risk arising from from derivatives. Like many other sovereign borrowers, Finland uses a collateral agreement (CSA, Credit Support Annex) under the ISDA framework agreement. A bilateral collateral agreement means that both parties are obligated to provide collateral against derivative positions.

Market risks

A key target variable for the interest rate risk management of the central government debt is the weighted average maturity at issuance (WAMI). For borrowing that has taken place after the current debt management directive entered into force in March 2024, the target for WAMI is on average seven years in the medium term. The weighted average maturity can deviate by up to six months from the aforementioned average maturity. For short-term borrowing, the calculation applies to the year-end debt stock and the average maturity of short-term issuance during the year. The WAMI of funding carried out in 2025 was 7.0 years.

The weighted average maturity at issuance (WAMI) of funding carried out in 2025 was 7.0 years.

The central government does not take on exchange rate risk in its debt management operations, and no exchange rate risk is associated with existing debt. While a portion of government borrowing is denominated in foreign currencies, all related exchange rate exposure is fully hedged through currency swaps.

Currency hedging involves collateral movements. In 2025, the government posted cash collateral as the euro appreciated against the US dollar. Posted cash collateral does not increase the central government deficit, but as it needs to financed, the posted collateral does increase the annual borrowing requirement. Until February 2024, the central government also used interest rate swaps to adjust its interest‑rate risk position, and the remaining contracts likewise involve collateral movements.

Collateral posted to counterparties is recorded as a receivable in the central government’s financial statements, as it will be returned when market value of the underlying derivate changes or when the contract expires. Conversely, collateral received from counterparties is recorded as a short‑term liability.

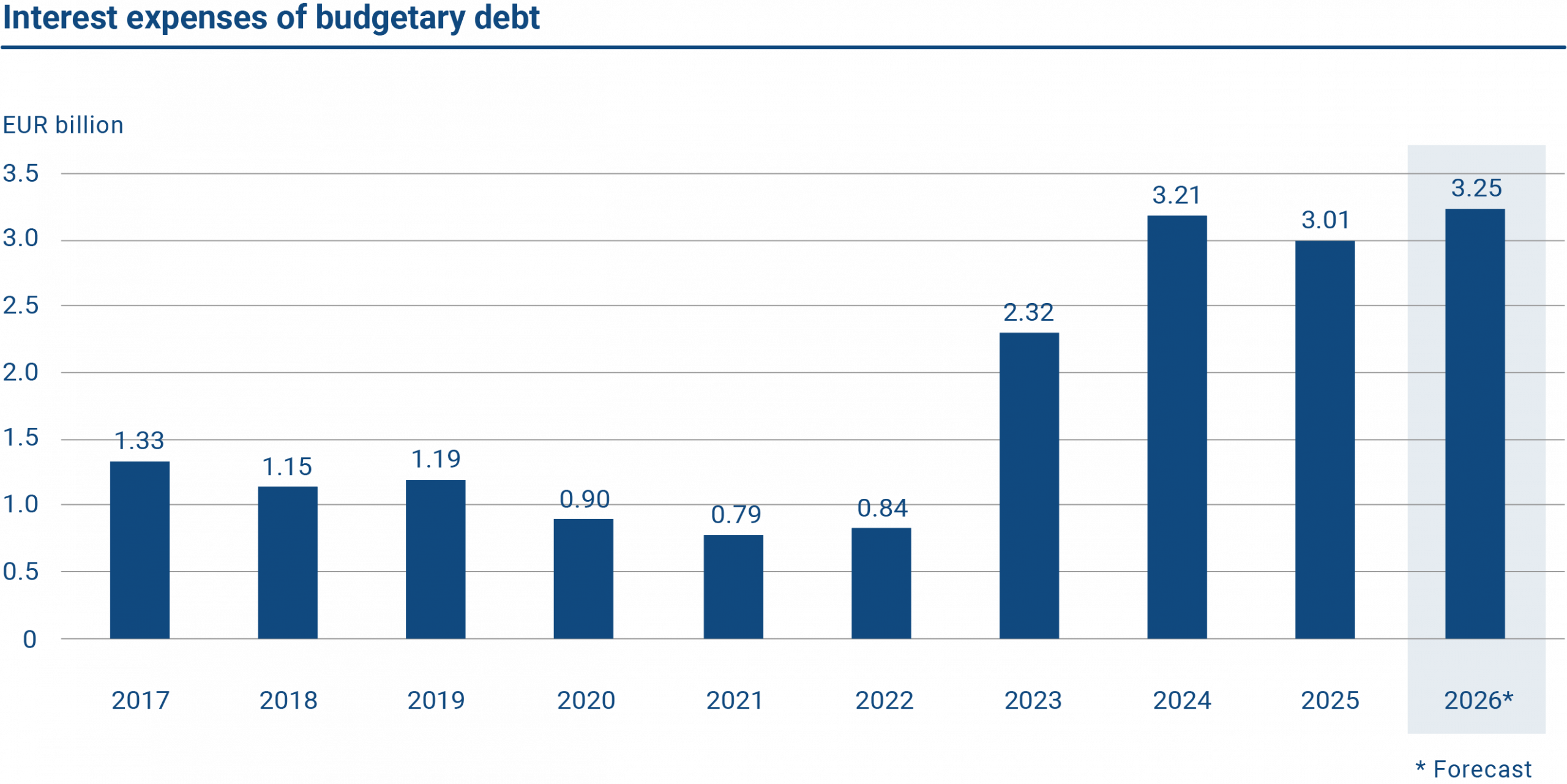

The graph shows the annual interest expenses of budgetary debt in 2017–2026. In 2025 the interest expenses were EUR 3.01 billion. The forecast for 2026 is EUR 3.25 billion.

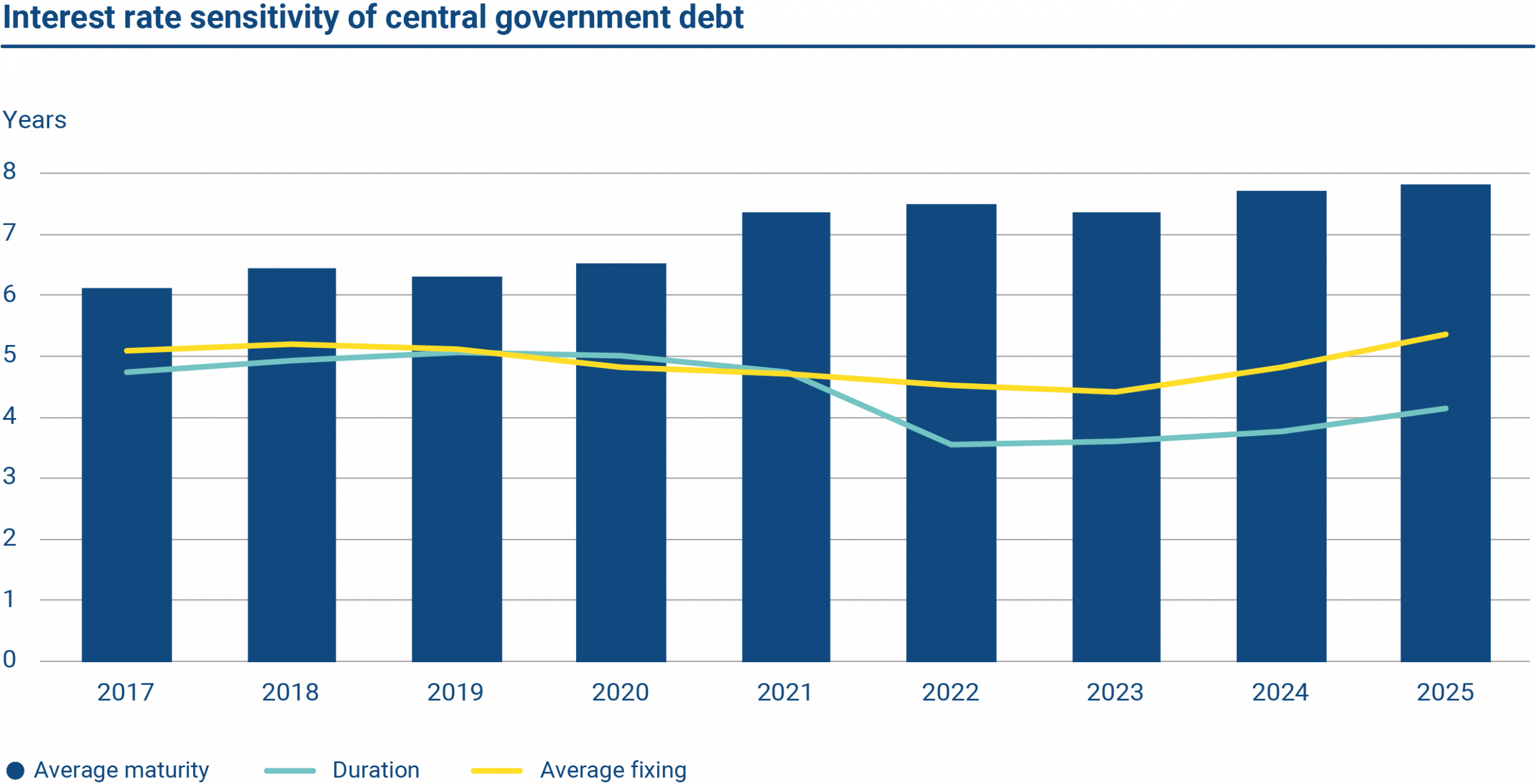

The graph shows the key figures on the interest rate sensitivity of central government debt. At the end of 2025, the average fixing of the central government debt was 5.39 years and duration 4.16 years. The average maturity was 7.84 years.

Operational risk

Operational risk means a risk arising from external factors, technology, or the inadequate performance of personnel, organisation or processes. A field requiring special attention is data security, which encompasses the security of both documents and IT systems. Equal focus is given to developing and continuously testing operative business continuity plans. Regular audits by external cybersecurity experts have also spurred improvements in operative processes.

The principles of operational risk management are implemented in daily operations. Incidence of realised risk events and near-miss incidents are compiled and reported to management. The State Treasury monitors risk factors and events regularly and makes risk assessments.

Legal risk

Legal risk is the risk resulting from failure to comply with laws and regulations or established market practices as well as invalidity, nullity, voidability, discontinuation or the lack of documentation of contracts, agreements and decisions.

The State Treasury has prepared a set of internal guidelines for the management of legal risks. The State Treasury actively monitors its legal operating environment and reacts to significant changes quickly when necessary.

The objectives of legal risk management are to ensure compliance with all applicable laws, rules and regulations and to minimize legal risk by utilising standard agreements and the government’s own templates. In addition, steps are taken to ensure that employees are familiar with legislation, regulations and market practices concerning their activities.

Internal control

Internal control is an integral part of management of the State Treasury. Internal control ensures the quality and efficiency of operational processes, the reliability of internal and external reporting, and compliance with laws and regulations. A sound system of internal control helps all parts of the organisation to reach their targets.

As part of internal control all main debt management processes are evaluated on an annual basis. The assessment pays special attention to the clarity of the State Treasury’s objectives, risks, and control procedures.