Economic activity in Finland did not expand as expected in 2025, showing only marginal improvement from the previous year. In particular, the increase in private consumption fell short of projections. In 2026, economic growth is forecast to strengthen to 1.1 per cent, supported by moderate inflation, rising purchasing power, and a gradual recovery in investment activity.

Finland’s gross domestic product (GDP) recorded only modest growth in 2025, with overall economic performance falling clearly short of expectations. The primary drag on growth was weak domestic demand. Household consumption failed to increase despite rising incomes. The construction sector remained in a downturn, and a more robust recovery would require a stronger rebound in the housing market. Consumer confidence was undermined by concerns related to the geopolitical environment, the current labour market situation, and uncertainties surrounding the fiscal adjustments required in Finland’s public finances.

The decline in consumer confidence has persisted for an exceptionally long period, prompting households to postpone purchases. This trend is reflected, for example, in the household deposit stock, which reached an all‑time high of nearly EUR 120 billion at the end of 2025. In addition, net household investment increased significantly over the course of the year.

The export sector, by contrast, performed more favourably in 2025. Global trade developments were supportive, and Finland’s exports expanded in line with international demand. The current account posted a slight surplus for the year. In addition, the overall investment rate began to show tentative improvement, with estimates indicating growth of just under two per cent in 2025.

Labour market conditions deteriorated during the year as unemployment rose sharply. This was no longer driven by a decline in the employment rate but rather by an expansion of the labour force. The increase in labour supply stemmed from immigration and government measures aimed at strengthening employment. At the same time, the employment rate remained relatively stable and even edged higher toward year‑end. By December, the trend employment rate for individuals aged 20 to 64 stood at 75.8 per cent, while the trend unemployment rate reached 10.7 per cent. Over the coming years, employment is expected to grow by an average of one per cent annually as economic conditions improve.

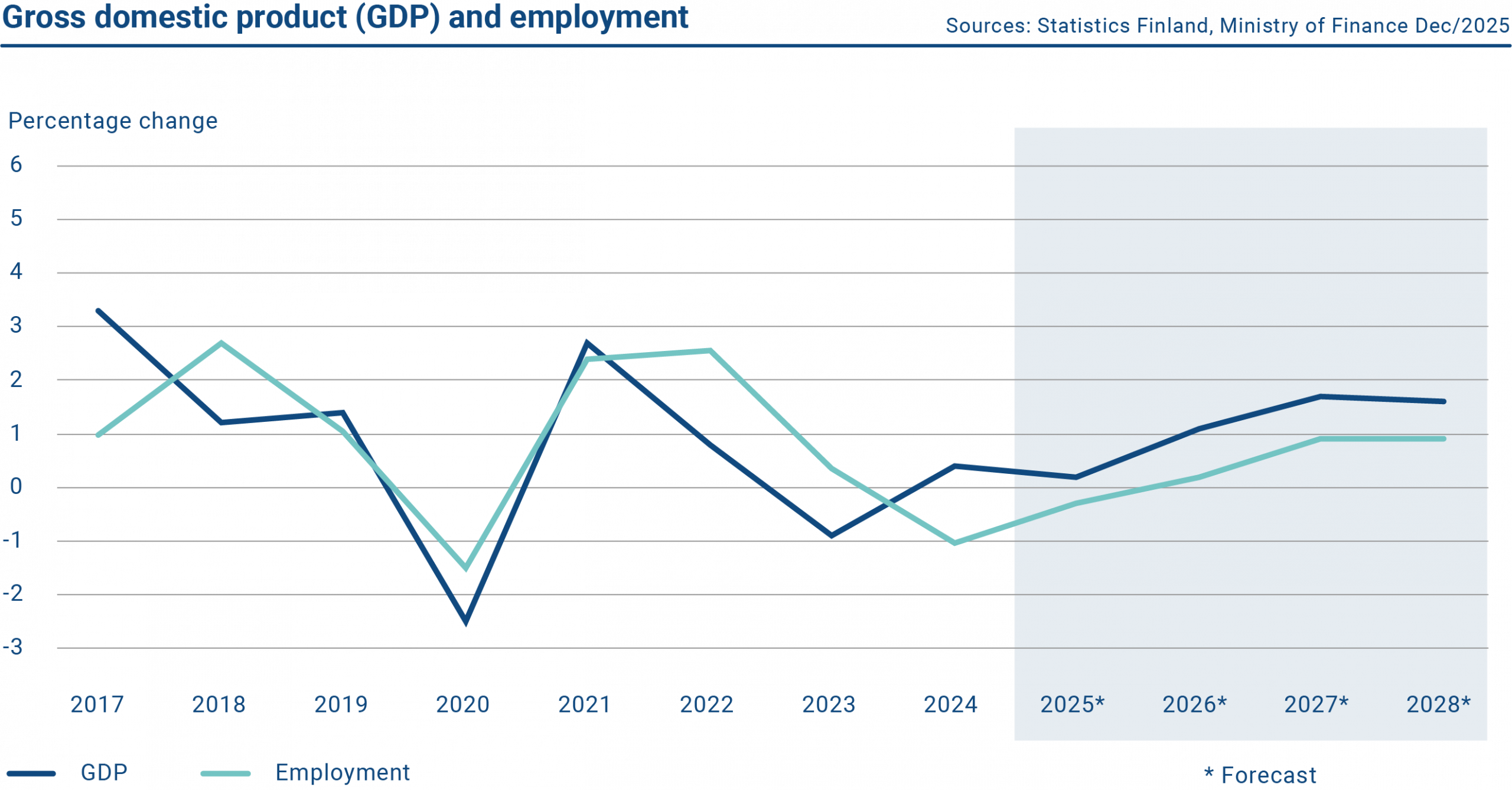

The graph shows information on the annual change in GDP and employment in Finland. In 2025 GDP grew and employment declined.

Public finances

Public finances faced considerable strain in 2025. Although the general government deficit narrowed during the year, it remained just below four per cent of GDP. The Government’s fiscal adjustment measures contributed to the improvement, yet the outlook for the coming years remains challenging. Public finances will continue to be affected by rising defence expenditure, higher interest costs, and only moderate economic growth. Finland’s general government debt ratio is already approaching 90 per cent of GDP. By contrast, central government debt remains significantly lower, standing at under 70 per cent of GDP in 2025.

The Republic of Finland has a solicited credit rating from S&P Global Ratings. At the end of 2025, the credit rating for long-term debt was AA+ with a stable outlook. Finland also has a number of other unsolicited credit ratings.

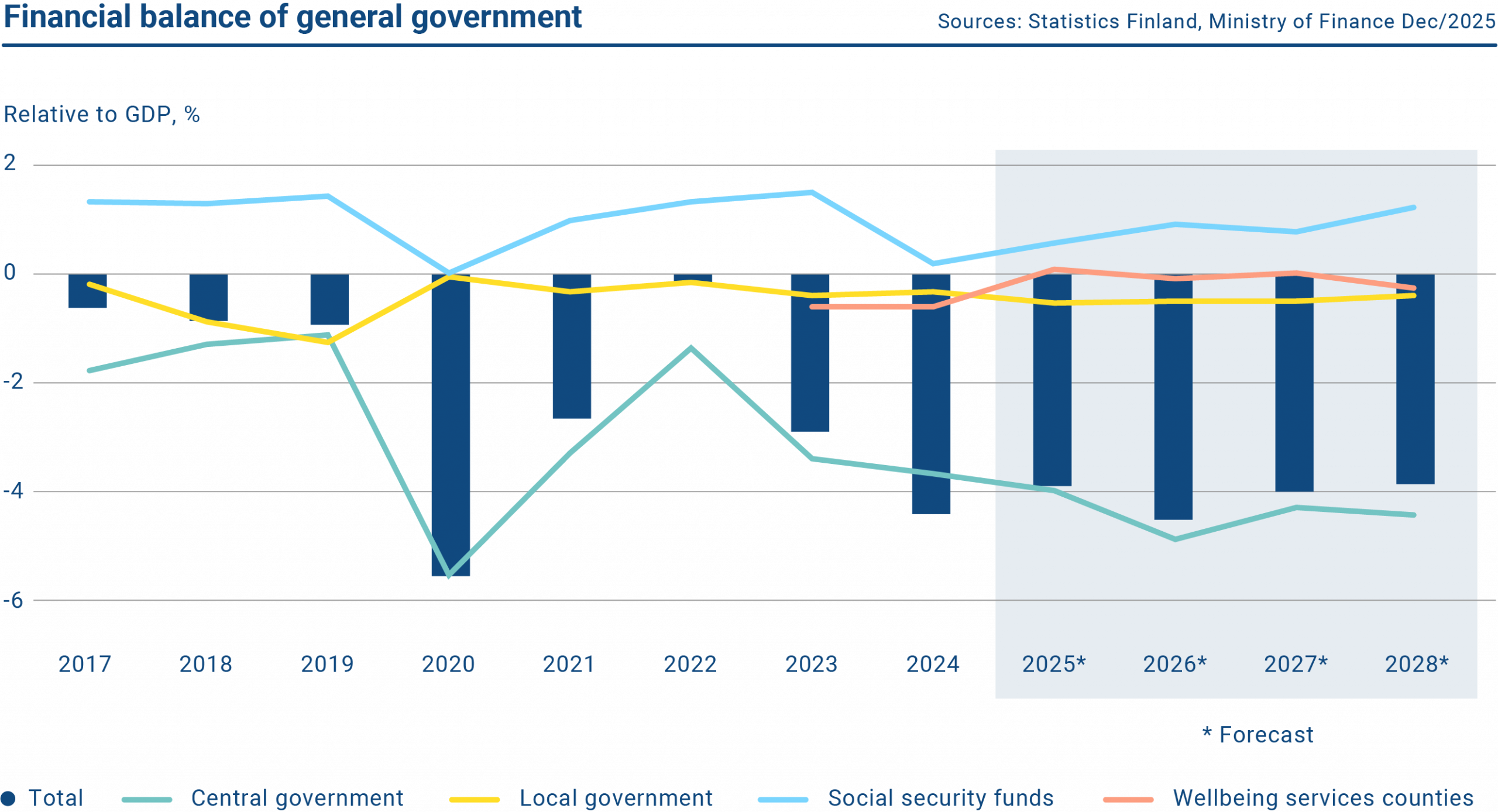

The graph shows the financial balance of the Finnish general government. Social security funds are running a surplus while central and local government show deficits.

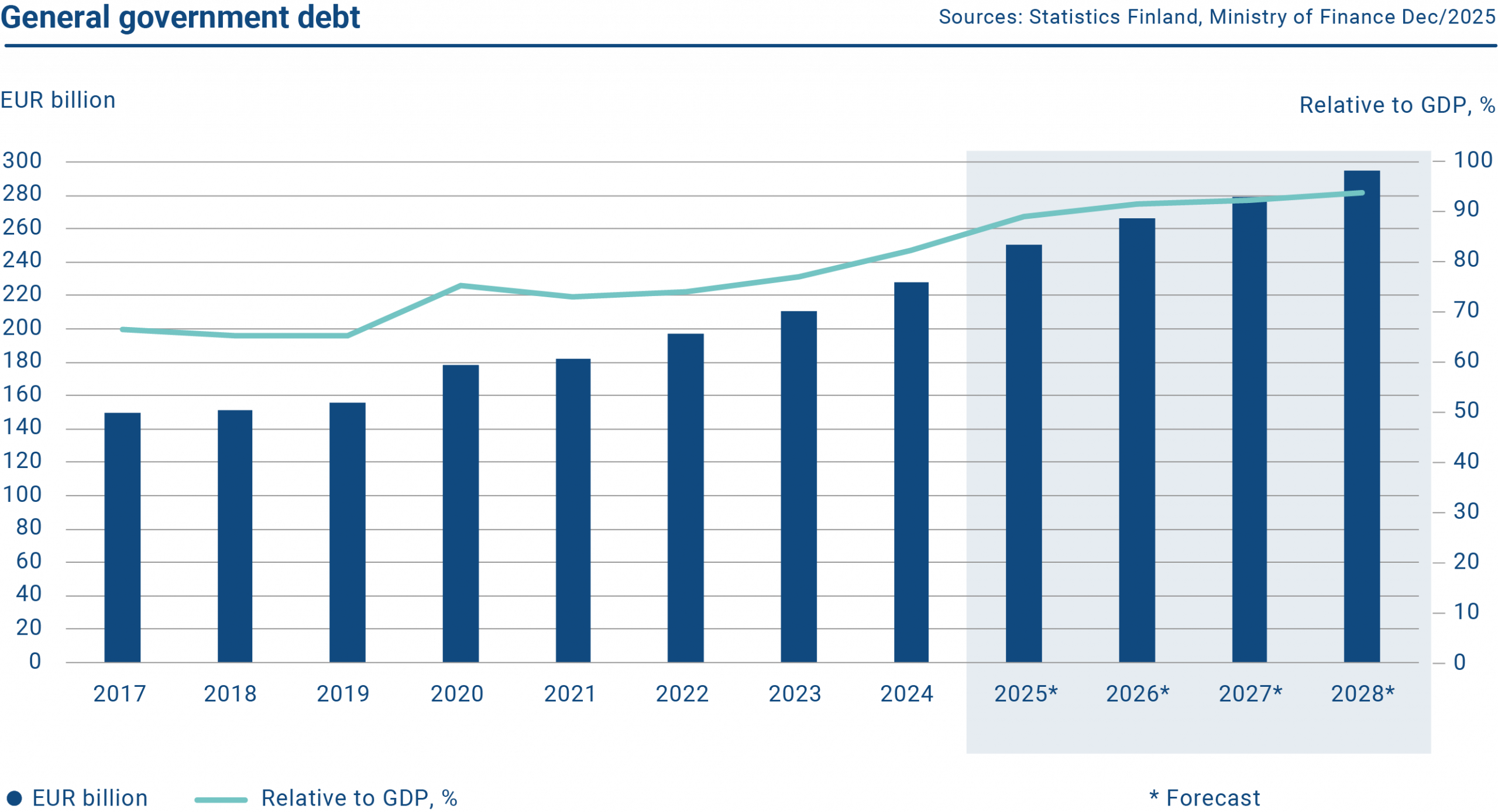

The graph shows the volume of Finland’s general government debt. In 2025, the general government debt was EUR 250.5 billion. The debt-to-GDP ratio was 89.1%.

Defence spending at 2.9% of GDP in 2025

In spring 2025, the Finnish Government announced its intention to raise defence spending to at least three per cent of GDP by 2029. As a NATO member, Finland has also committed to the Alliance’s collective objective of increasing defence expenditure to five per cent of GDP by 2035, with core defence spending accounting for 3.5 per cent of the target. The remaining 1.5 per cent is allocated to defence‑related expenditure such as civil preparedness, infrastructure, and cybersecurity.

Defence spending in 2025 rose close to the three‑per‑cent threshold. Expenditure in the coming years will continue to reflect the substantial F‑35 fighter procurement, valued at approximately EUR 10 billion. Preparations for the acquisition began in the mid‑2010s, and the Government approved the purchase in December 2021. The programme will continue to influence Finland’s defence budget through 2031. In response to the shifting geopolitical environment, the Government has also committed to significant additional investments in internal security and has accelerated the launch of the Army’s modernisation programme.

The timing of defence procurements and related deliveries introduces considerable uncertainty into the general government balance, particularly for central government finances. The public‑sector deficit in 2025 was smaller than expected (3.9 per cent), but according to the Ministry of Finance, it is projected to widen to 4.5 per cent in 2026, as fighter aircraft deliveries originally anticipated for 2025 will be recorded only next year. Because no deliveries were booked last year, subsequent years will see correspondingly higher entries.

Finland’s defence expenditure is expected to remain elevated. While high defence spending places pressure on the central government’s fiscal position, defence investments are also anticipated to support economic growth. Public backing for increased defence expenditure remains strong among Finns.

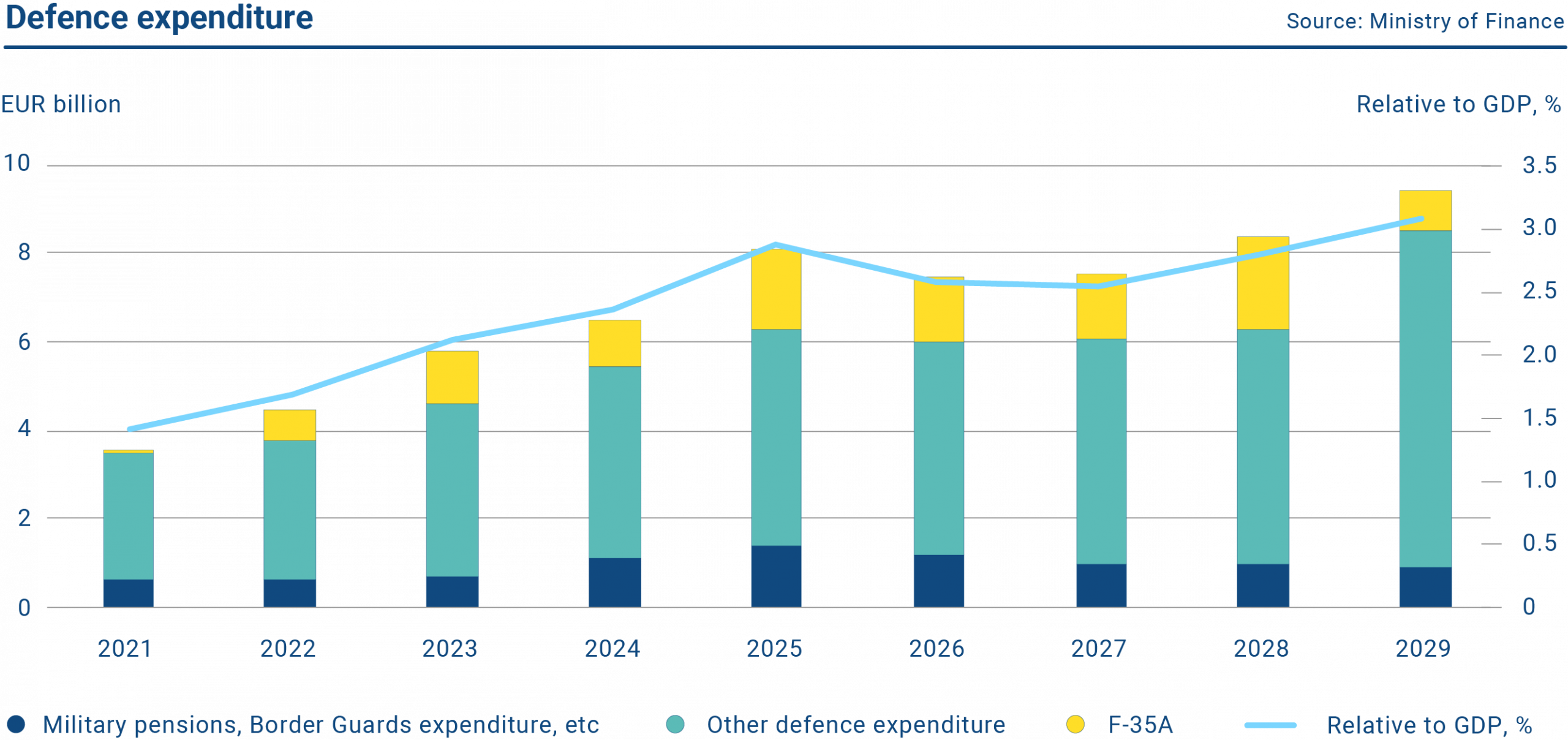

The graph shows the development of Finland’s defence spending from 2021 to 2025, as well as a forecast for 2026–2029. In 2025, Finland’s defence expenditure was estimated at 2.9% of GDP.

Interest rate developments

Monetary policy continued to ease across several major economies in 2025. As inflationary pressures subsided, the European Central Bank (ECB) proceeded with a series of rate cuts. By June, the ECB had lowered the deposit facility rate four times by 0.25 percentage points, bringing it to 2.00 per cent. In the United States, the Federal Reserve lowered its key policy rate three times between September and December, each time by 0.25 percentage points. By year‑end, the federal funds rate had moved into the target range of 3.50–3.75 per cent.

Finnish government bond yields fluctuated throughout the year. The yield on the 10-year benchmark bond rose early in the year, stabilised over the summer, and resumed a moderate upward trend in the autumn. The yield stood at 2.85 per cent at the beginning of 2025 and ended the year at 3.16 per cent.

The graph shows the 10-year government bond yields of Germany, Finland and the United States in 2015–2025.

The conclusion of the ECB’s purchase programmes, combined with substantial borrowing needs across Member States, kept the supply of government bonds elevated. This contributed to historically high yield levels on central government debt relative to swap rates. The dominant themes in the 2025 government bond market—namely the steepening of the yield curve and the rise in ultra‑long rates—were driven by large fiscal deficits and heightened geopolitical tensions. The 30‑year swap rate increased by more than 100 basis points during the year, with long‑term government bond yields rising by nearly the same magnitude. Finland’s 30‑year yield climbed from 3.10 per cent at the start of 2025 to 3.88 per cent at year‑end.

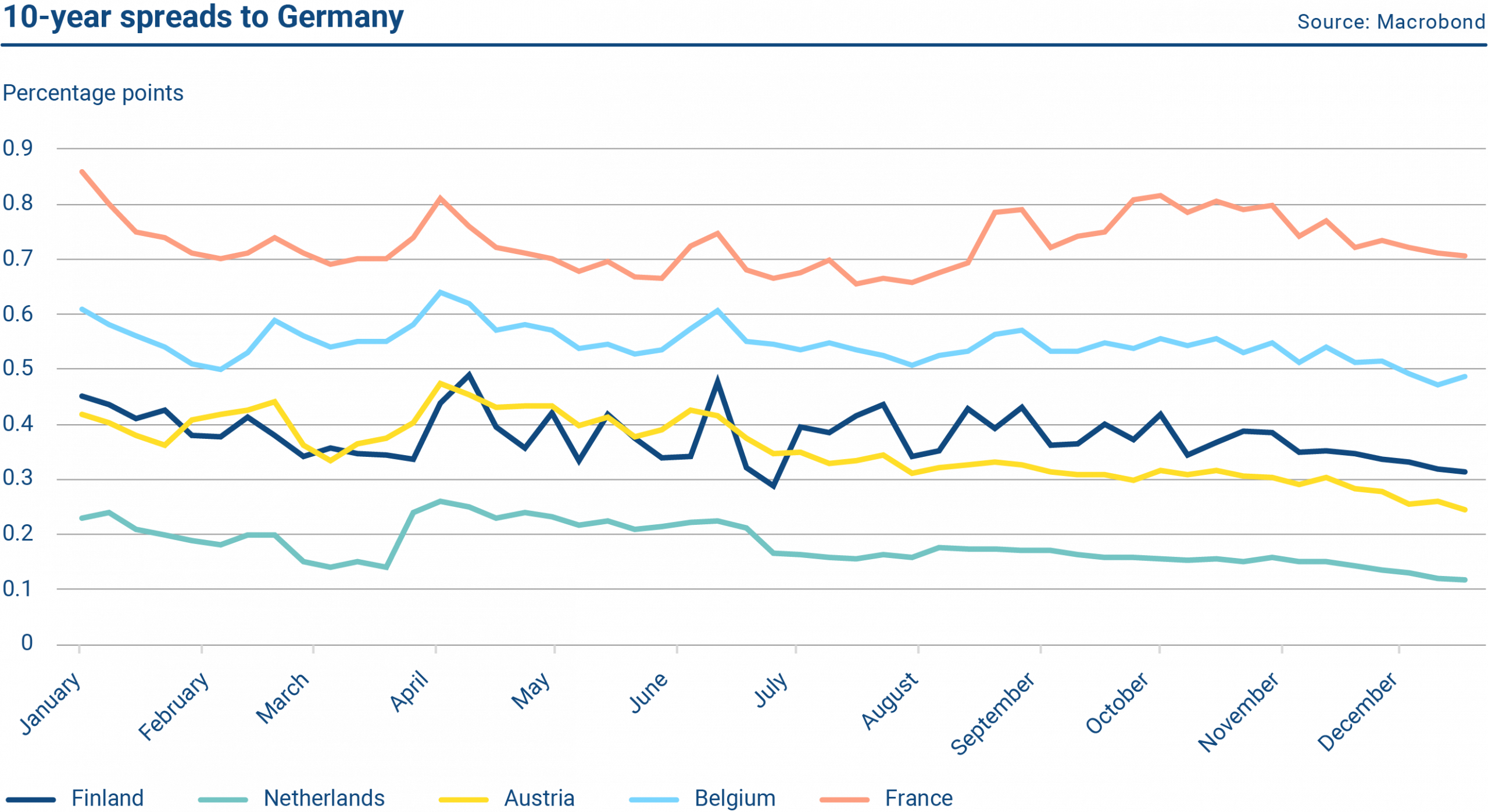

Yield spreads among euro area countries, both relative to Germany and to one another, also moved somewhat over the course of the year. Following Germany’s announcement of substantial investments to defence and infrastructure, German government bond yields rose, tightening the spreads between Germany and other euro area sovereigns. The compression was particularly pronounced in Southern Europe—Spain, Portugal, Italy, and Greece—where economic growth outpaced that of Northern Europe and credit ratings were upgraded. Finland’s ten‑year spread to Germany tightened by roughly 15 basis points over the year, with similar movements observed in other key reference countries such as the Netherlands and Austria.

The graph shows the 10-year bond spreads of Finland, the Netherlands, Austria, Belgium and France against Germany.

Secondary market developments

The strong liquidity of government bonds enables investors to execute transactions quickly without exerting significant pressure on prices. Maintaining and further enhancing the liquidity of Finnish government benchmark bonds remains a key priority for the State Treasury, which works closely with its Primary Dealers to support efficient market functioning. Finnish government bonds are generally regarded as having good liquidity, which continues to underpin strong investor demand.

The graph shows the Primary dealers of the Republic of Finland in 2025.

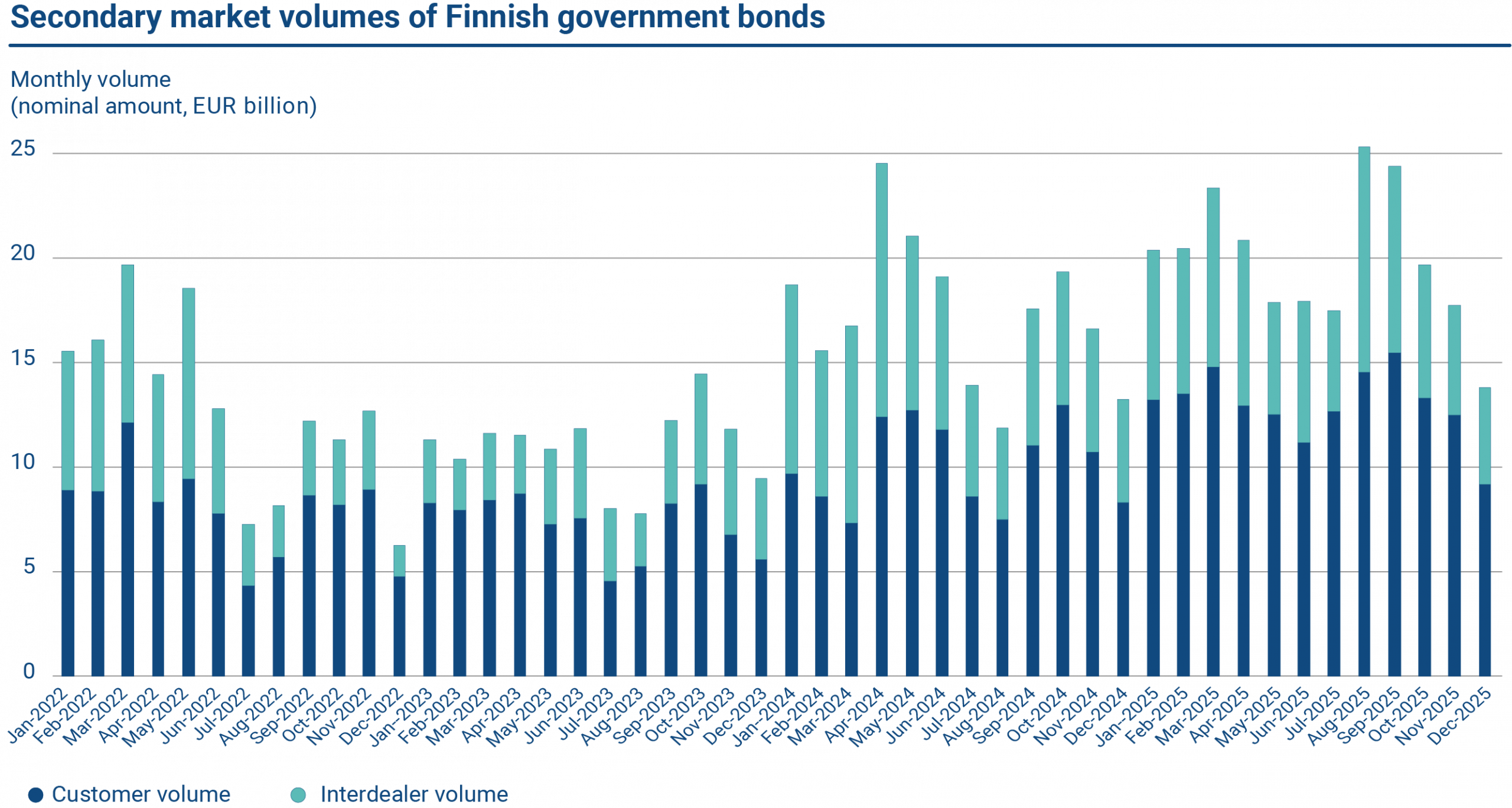

Secondary market activity increased in 2025 compared with the previous year. Total annual turnover reached EUR 155.2 billion, up from EUR 121.3 billion in 2024. Average monthly turnover (combined purchases and sales) amounted to EUR 13.0 billion, compared with EUR 10.1 billion a year earlier. In relative terms, the monthly average turnover corresponded to 7.9 per cent of the outstanding euro‑denominated benchmark bond stock (7.0 per cent in 2024).

Finnish government benchmark bonds are traded on the MTS Finland and BrokerTec interdealer platforms. The State Treasury does not participate in secondary‑market trading; activity is driven by Primary Dealers and other market participants. In 2025, nominal interdealer trading volumes averaged EUR 7.0 billion per month, compared with EUR 7.2 billion in 2024.

The graph shows the secondary market volumes of Finnish government bonds in 2022–2025. In 2025, the nominal interdealer trading volume was on average EUR 6.95 billion per month. The average monthly customer volume was EUR 12.95 billion.

The State Treasury closely monitors Primary Dealer quoting activity in the secondary market. It has established quoting guidelines for different maturities in the interdealer market, where bid–offer spreads are systematically observed and tracked. The average bid–offer spread across all market makers is calculated, and each Primary Dealer is benchmarked against this average. The State Treasury provides weekly feedback to individual Primary Dealers by reporting the analysed spread data for benchmark bond quotes. Reflecting the tightening of bid–offer spreads, the liquidity of Finnish government benchmark bonds improved in 2025 compared with the previous year.