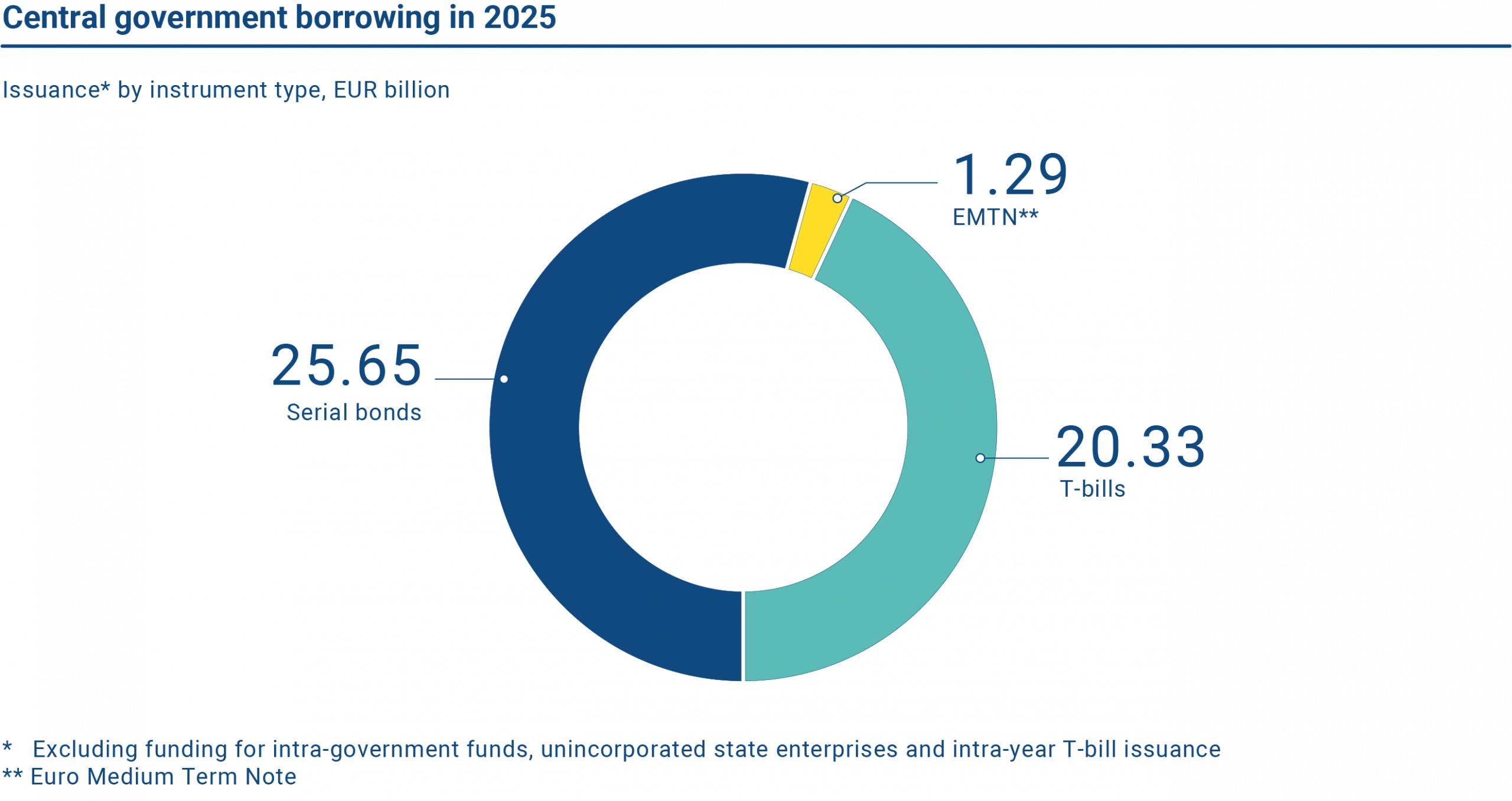

In 2025, the Republic of Finland’s realised gross borrowing totaled 47.3 billion euros. Of this amount, long-term issuance accounted for EUR 26.9 billion (57%). The rest, EUR 20.3 billion (43%) was short-term borrowing. Realised net borrowing amounted to EUR 17.8 billion.

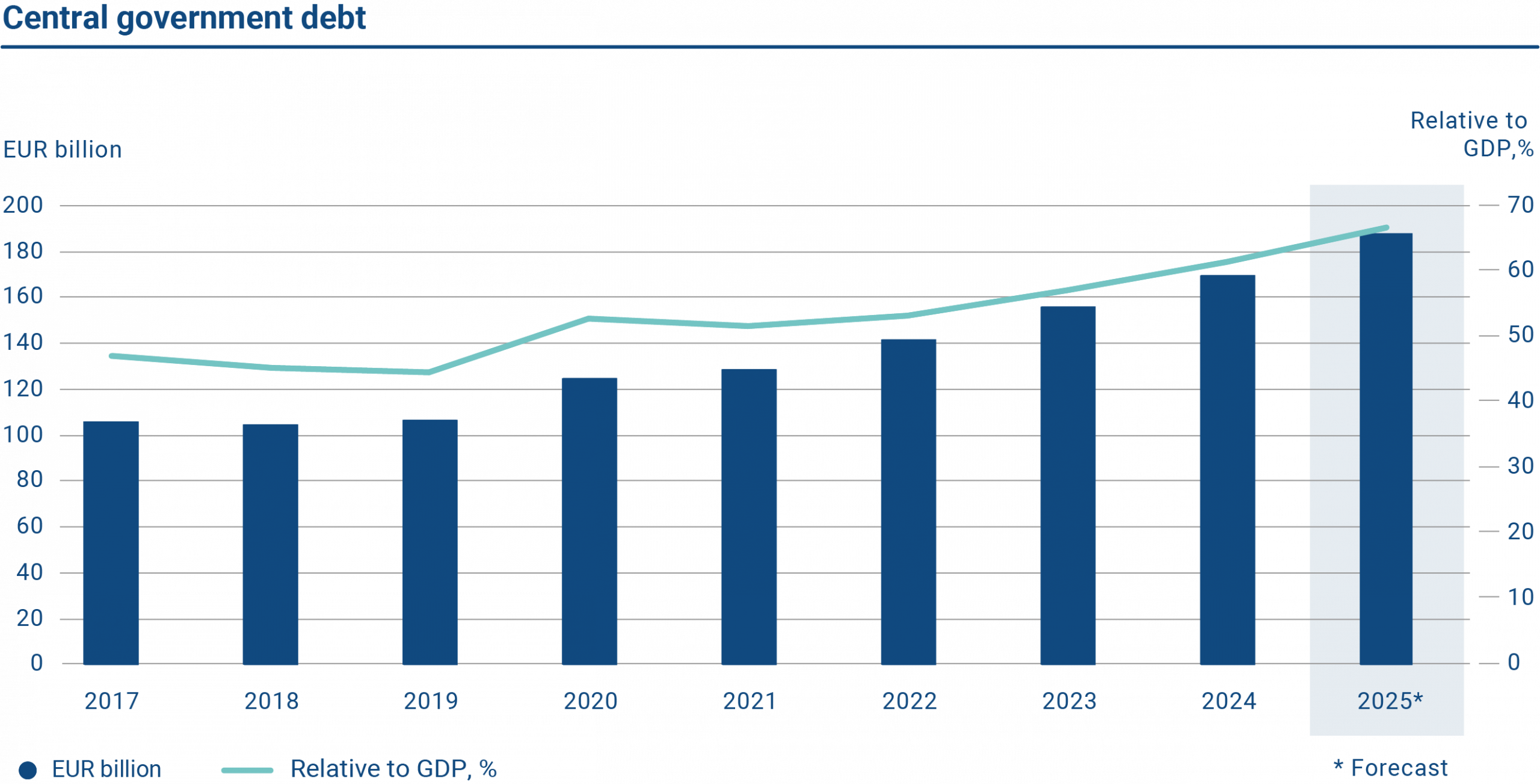

The central government’s gross borrowing requirement will remain at around EUR 40–45 billion euros in the coming years. At the end of 2025, central government debt stood at EUR 188 billion.

The realised gross borrowing amount in 2025 was EUR 47.26 billion. Of this amount, long-term issuance accounted for EUR 26.93 billion and short-term borrowing for EUR 20.33 billion.

The realised gross borrowing amount in 2025 was EUR 47.26 billion. Of this amount, long-term issuance accounted for EUR 26.93 billion and short-term borrowing for EUR 20.33 billion.

The graph shows the volume of Finland’s central government debt and debt in relation to GDP in 2017–2025. The central government debt was EUR 187.67 billion at the end of 2025. The debt-to-GDP ratio was 66.70%.

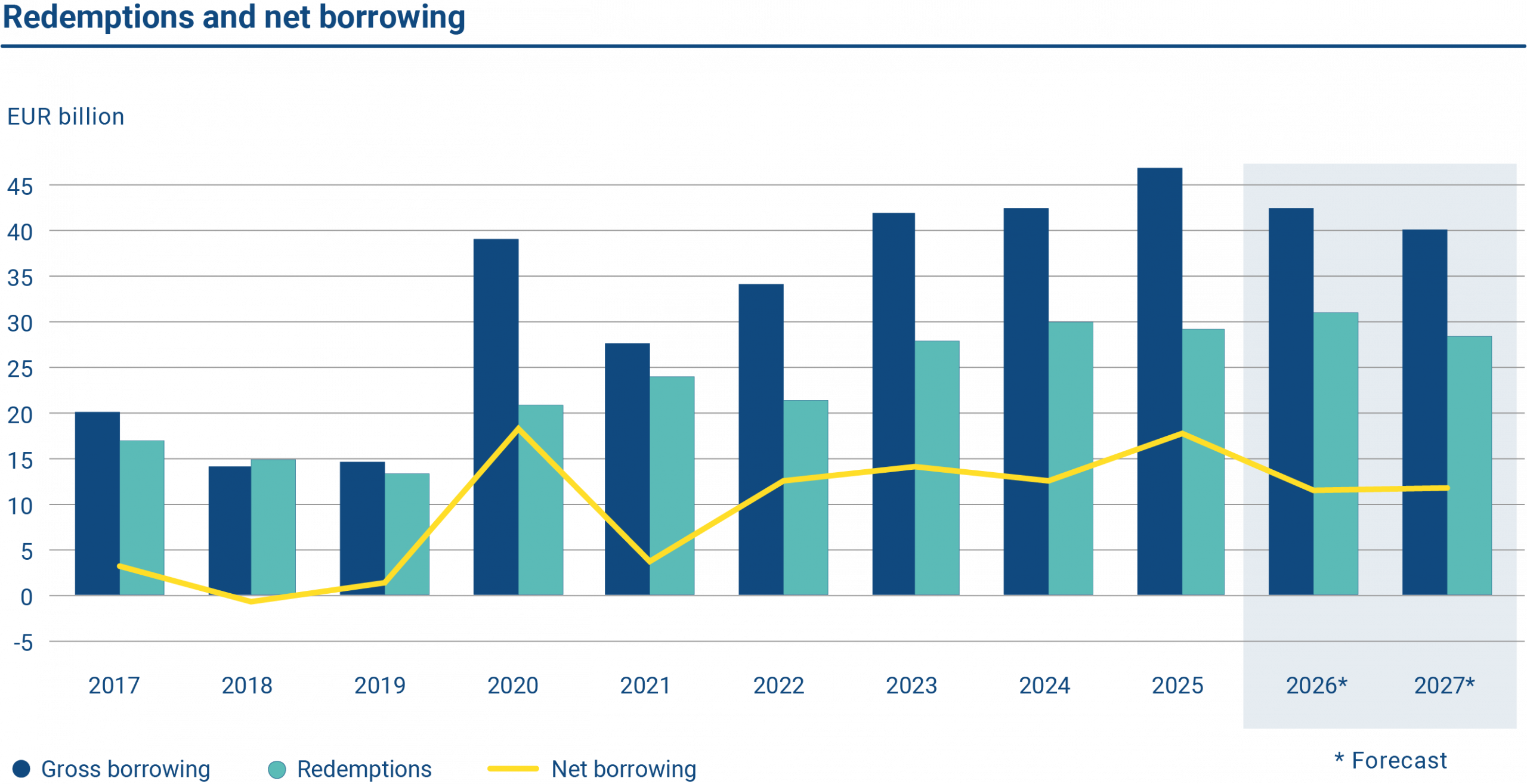

The graph shows annual gross borrowing, redemptions and net borrowing in 2017–2027. Redemptions of EUR 29.46 billion took place in 2025 while net borrowing amounted to EUR 17.80 billion.

The budgeted central government net borrowing requirement for 2026 is EUR 13.1 billion. With EUR 31.1 billion of redemptions, the gross borrowing requirement totals EUR 44.2 billion.

Funding strategy

The funding strategy of the Republic of Finland is based on euro benchmark bond issuance. Benchmark‑based funding in the wholesale market is cost‑efficient for a sovereign, as benchmark bonds benefit from large outstanding volumes. Primary issuance helps establish a broad and diversified investor base, while market‑making supports price discovery and ensures liquidity in the secondary market.

New benchmark bonds are issued in syndicated form. Syndications are supplemented by regular tap auctions, which further increase the outstanding volumes of established bond lines. There is also a Euro medium-term note (EMTN) programme under which the Republic of Finland can issue bonds in foreign currencies to serve a broader investor base. However, issuance in foreign currencies is subject to market conditions and a reasonable funding cost in comparison to euro issuance.

The current funding volume supports three new euro benchmark bond syndications per year, tap auctions of existing benchmark bonds, and one benchmark-sized USD bond issuance. The short-term funding is carried out by issuing Treasury bills. In terms of bond maturities, the annual issuance pattern of a new 10-year bond is complemented with a new long-term bond – either 15, 20 or 30 years – to maintain a liquid benchmark bond curve up to 30 years. This year, subject to market conditions, the State Treasury will issue a new 15-year benchmark bond. The third new issue of 2026 will most likely be launched in the 5–7‑year segment to maintain a balanced redemption profile. Market conditions permitting, issuance in currencies other than euro, most likely a USD benchmark bond, may complement the long-term funding. The share of short-term funding, i.e. Treasury bills, is estimated to be around 40% of annual gross borrowing.

The objective of the State Treasury is to maintain Finland’s position as a recognised and reliable issuer in the markets and thus ensure the demand for Finnish government bonds in the future.

Funding operations and investor demand

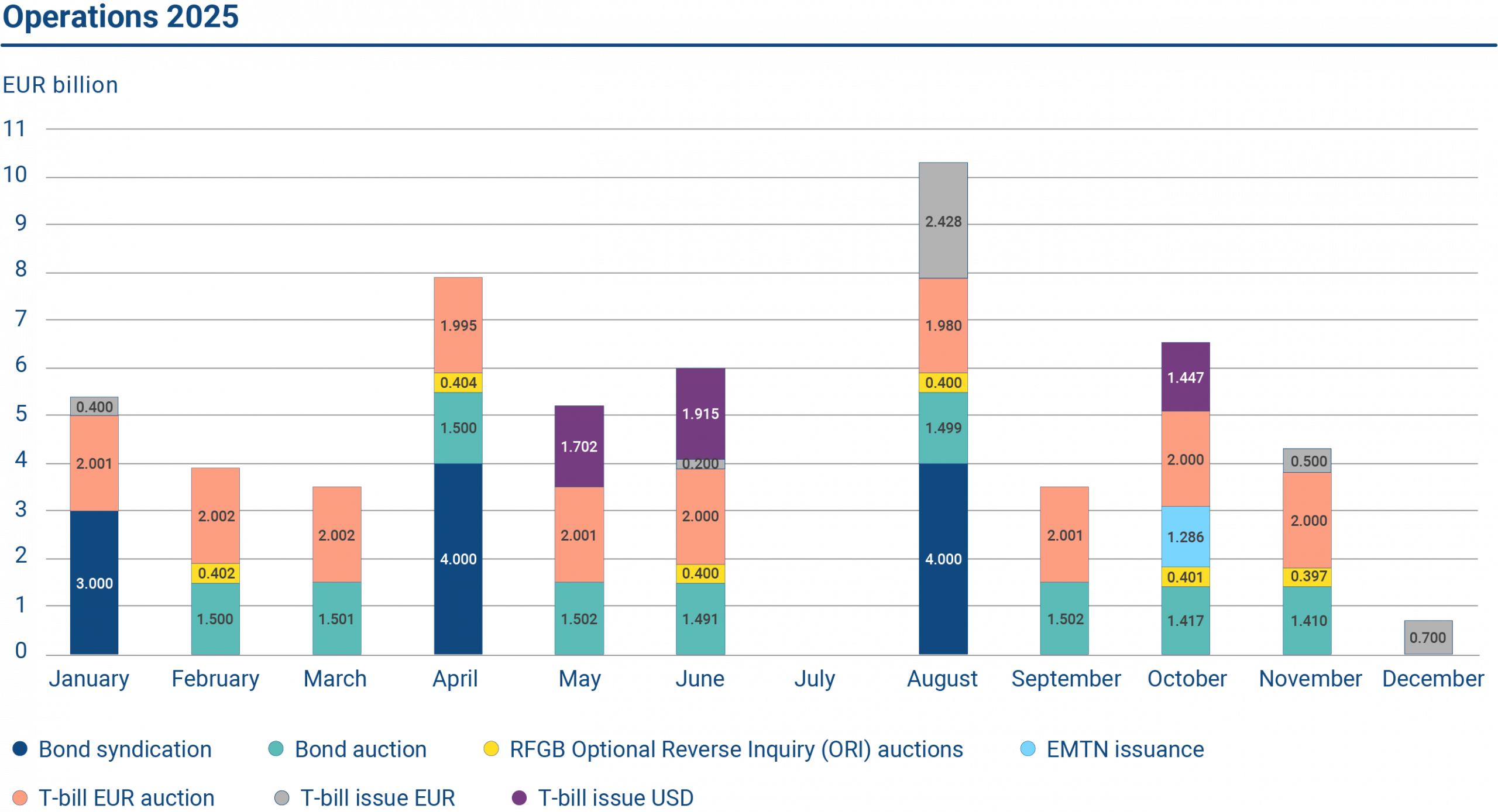

In 2025, the Republic of Finland issued three new euro‑denominated benchmark bonds and one USD‑denominated benchmark. A total of 15 benchmark bond auctions were conducted during the year. Short‑term funding was carried out by issuing Treasury bills in auctions and in ECP format.

The graph shows the operations conducted by the State Treasury in 2025 Finland issued three new euro-denominated benchmark bonds, one USD-denominated bond, and arranged nine regular bond auction. The short-term funding was carried out by issuing Treasury bills.

The first syndicated bond issue of the year took place in January when Finland raised EUR 3 billion with a new long 20-year benchmark bond. The bond matures on 15 April 2045 and pays an annual coupon of 3.2%. As customary, the top five performing Primary Dealer banks of the previous year were appointed as lead managers for the issue, and the other primary dealers as co-leads. The bond attracted a record demand, building an order book of over EUR 31 billion from 220 investors. The new long‑dated bond had strong asset manager and pension fund participation.

The second syndicated transaction in late April was, as expected, a new 10‑year benchmark bond with a maturity date of 15.9.2035. The bond was priced at 52 basis points over the euro swap curve to yield 3.016%. The order book exceeded EUR 23 billion and included offers from more than 150 investors. The broad-based demand allowed upsizing the deal to EUR 4 billion at issuance. Nearly 40% of the bond was allocated to central banks and official institutions.

The third euro-denominated syndicated issue of 2025 was a new 7‑year benchmark due 15 April 2032, issued in August. The bond was priced at 29 basis points above the euro swap curve, with a yield of 2.751%. The order book grew to over EUR 33 billion and included orders from 160 investors. The depth of the order book and the substantial participation of long‑term investors again allowed the transaction to be upsized from EUR 3 billion to EUR 4 billion.

In October, the Republic of Finland visited the dollar market by raising $1.5 billion with a new USD‑denominated bond. The bond has a maturity date of 4.11.2030. The yield at issuance was 3.684%, which was 37 basis points above the mid‑swap rate (USD SOFR) and 6.6 basis points over the pricing reference of UST due 31 October 2030. This was Finland’s second US‑dollar issuance in the past five years. Issuing in US dollars complements Finland’s euro-denominated borrowing with the purpose of serving a more global investor base.

The graph shows all outstanding serial bonds issued by the State Treasury. Of these, the majority are benchmark bonds.

Who did Finland borrow from in 2025?

In 2025, Finland issued three new euro‑denominated benchmark bonds and one US‑dollar bond, raising a total of EUR 12.3 billion. Order books were heavily oversubscribed across EGB bond syndications in 2025, including Finland’s. This allowed the State Treasury, in coordination with the joint lead managers, to allocate the bonds across investor categories in line with predefined principles.

The investor base for Finnish central government debt is largely European. In 2025, more than 80 per cent of the new syndicated issuance was sold to investors in Europe. The Nordics, the United Kingdom and Central Europe form the traditional regional core of Finland’s investor base. Domestic investors accounted for 6 per cent. By investor type, the majority of the allocation – 87 per cent in total – was placed with central banks and other official institutions, banks and bank treasuries, as well as asset managers.

The graph shows syndicated issuance participation in 2025 by investor type and region.

Auctions

In addition to the syndicated issuances, the State Treasury conducts tap auctions on existing benchmark bonds in the primary market. An auction calendar is published quarterly on the State Treasury website. In 2025, nine regular benchmark bond auctions and six optional reverse inquiry (ORI) auctions were conducted in total. ORI auctions were continued in response to the positive feedback received. The purpose of the facility is to support the RFGB secondary market liquidity, by providing an opportunity for market makers to source off-the-run bonds in the primary market regularly.

All auctions were used to increase the outstanding volumes of existing benchmark bonds. Of the regular auctions, five were held in the first half of the year and four in the second half.

The total auctioned funding volume in 2025 via benchmark bond auctions was EUR 15,726 million, of which EUR 2,404 million were from ORI auctions. All auctions were dual line auctions including two bonds with different maturities. The bid‑to‑cover ratios for the auctioned securities, reflecting investor demand, varied from 1.11 to 1.92 (excluding ORI auctions). The issued amounts were between EUR 548 million and EUR 874 million per bond per auction (excluding ORI auctions).

The table shows serial bond auctions.

Short‑term funding

The State Treasury issues Treasury bills in euros and US dollars through banks included in the Treasury Bill Dealer Group. Short‑term funding is carried out according to the financing needs of the central government.

Euro‑denominated Republic of Finland Treasury bills (RFTBs) are issued via auctions. In auctions, the counterparties belonging in the Treasury Bill Dealer Group can submit bids. These auctions are uniform price by format, which means that the State Treasury determines the cut-off rate. All bids submitted at rates lower than the cut-off rate are allocated in full.

In 2025, the State Treasury organised ten Treasury bill auctions, raising a total of EUR 19,982 million.

The table shows Treasury bill auctions.

The State Treasury may also issue Treasury bills on other occasions, depending on demand and financing needs, in which case the State Treasury sets the yield for the issue. This issuance method resembles that of Euro Commercial Paper programmes (ECP). Treasury bills in ECP format can be issued in two currencies: in euros and in US dollars.

In 2025, ECP format Treasury bill issuance was conducted both in USD and EUR based on pricing and demand during the year. The gross ECP issuance is USD was 6.0 billion and in EUR 4.2 billion.

The average maturity in USD ECP issuance was 6.2 months and EUR ECP issuance 7.6 months. At the end of 2025, the outstanding stocks of USD- and EUR-denoninated Treasury bills were USD 4,000 million and EUR 17,192 million (corresponding figures for 2024: USD 4,120 million and EUR 15,380 million).

Liquidity management

The amount of central government cash reserves varies daily depending on income and expenditure flows. The size of the central government’s cash buffer is based on an assessment of sufficient liquidity and limits on uncovered net cash flows. Cash flows follow both intra-month and annual seasonal patterns due to timing mismatches in income and expenditure. Changes in the budget deficit during the fiscal year also affect liquidity management via changes in borrowing requirements.

As the primary focus is sufficient liquidity, actual borrowing may deviate from that budgeted for the fiscal year for various reasons, e.g. deferrable allowances which are budgeted in a specific year but used over a number of years. In 2025, the actual net borrowing (EUR 17.8 billion) exceeded the budgeted amount (EUR 14.3 billion) by an exceptionally large margin of EUR 3.5 billion. The increased borrowing need was driven by debt‑management factors, particularly the rise in cash collateral requirements linked to interest rate and currency derivatives

The central government’s derivative contracts include collateral arrangements to reduce credit risk. In 2025, Credit Support cash collateral posted by central government increased by EUR 3.3 billion compared with the end of 2024. The increase was due to changes in interest rates – especially the steepening of the yield curve (i.e. growth of the difference between long- and short-term interest rates) – as well as the appreciation of the euro against the US dollar. The amount of collateral changes daily according to movements in the market value of the underlying derivatives.

Cash collateral transactions are managed as part of the central government’s cash management operations. Cash collateral posted by the central government is returned upon the expiry of each contract at the latest. The central government earns interest income on the collateral it provides.

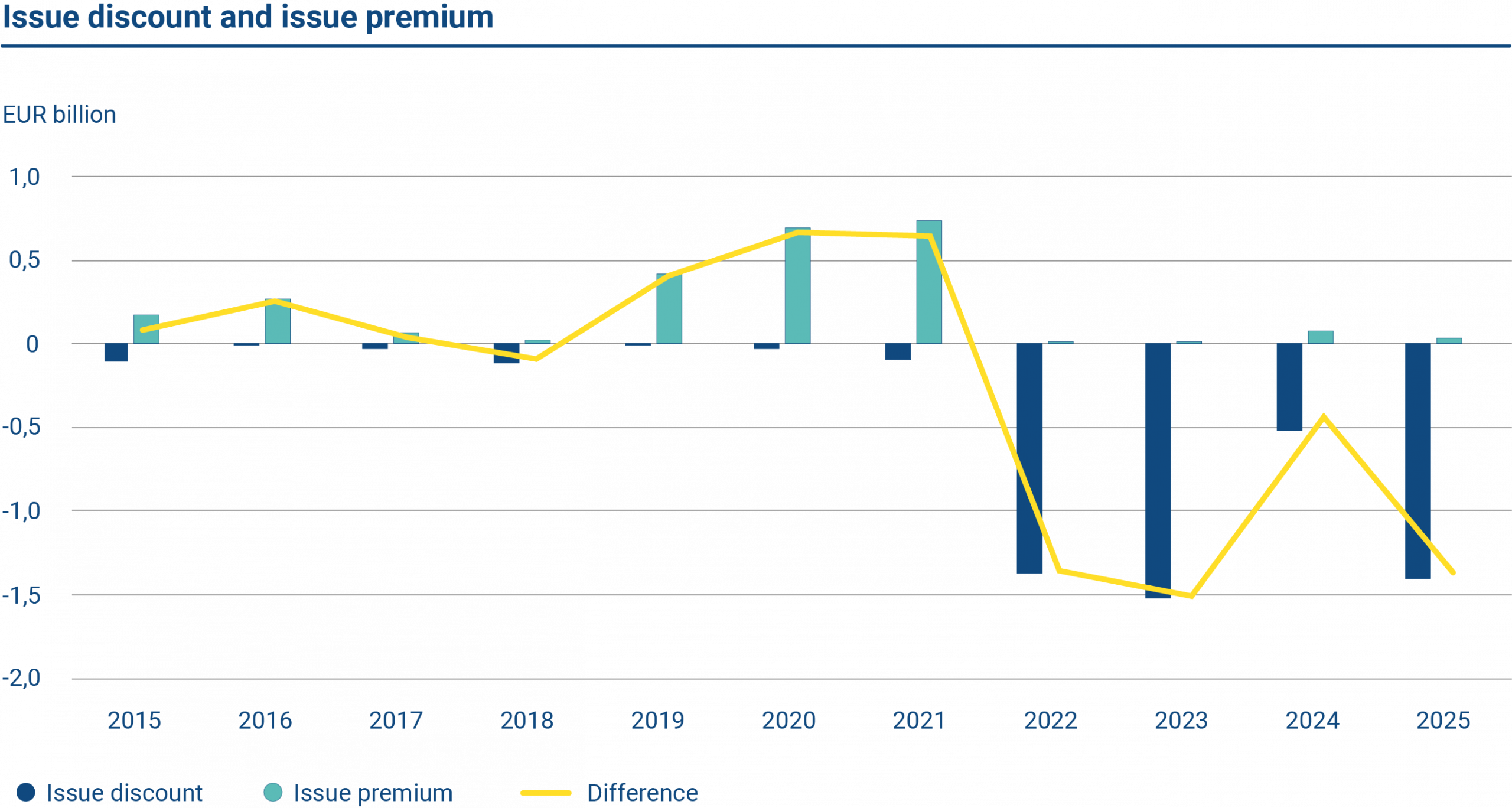

What does bond price variance from par mean?

In 2025, issuing some benchmark bonds below par, i.e. the bond’s nominal value, resulted in an increase in nominal issuance and thus nominal borrowing. In accounting, bond issue premia and discounts are referred to as valuation accounts or amortizing items. These do not reflect any profit or loss of the activity but adjust the carrying value of the bond on the balance sheet.

Issue discounts are a feature of issuing fixed rate bonds with coupon rates – which reflect market rates at first issuance – below current market rates. This means the issue price and thus issue proceeds are below par while the running interest cost is lower than the current market rate.

On net terms, cumulative bond amortizations have been issue discounts since 2022. Prior to that, they were issue premia meaning issue proceeds exceeded bond nominal values when coupon rates were higher than market rates at the time of issuance.

The graph shows the issue discount and issue premia of central government borrowing in 2015–2025.

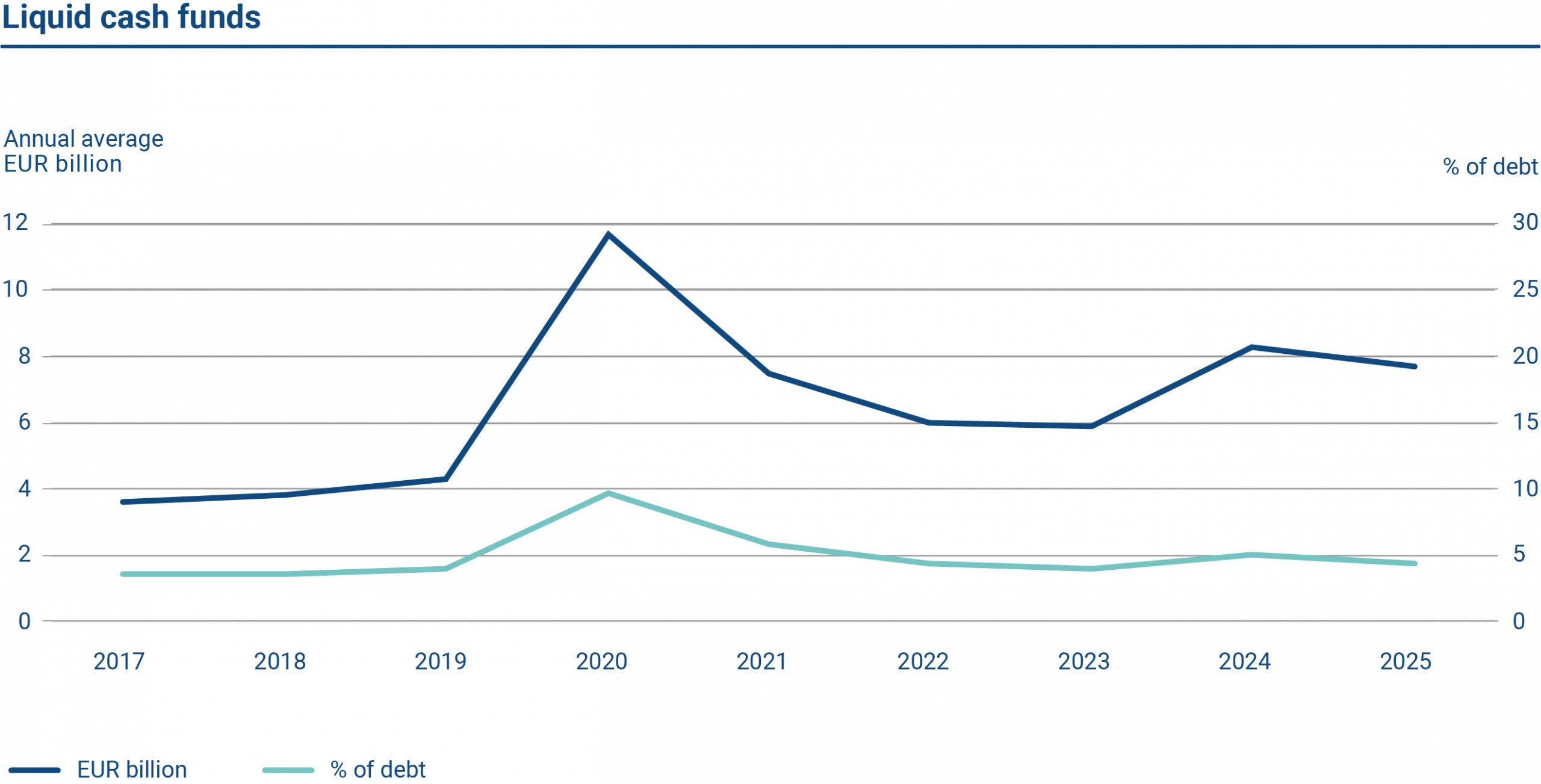

Central government’s cash reserves are invested in very short-term maturities using primarily bank and central bank deposits and triparty repos. Triparty repos are deposits made with approved counterparties and secured by high‑quality collateral, with collateral management handled by a third party such as a central securities depository.

Liquidity management relies on the central government cash flow forecast system. All government accounting entities forecast their income and expenditure for the next 12-month period into the system. The State Treasury uses this data as a basis for liquidity management decisions. In 2025, the central government’s average month‑end cash balance was EUR 7.7 billion.

The annual average of liquid cash funds was EUR 7.7 billion or 4.3% of debt in 2025.