Finland is currently one of the most rapidly ageing countries in the EU, but within the next 25 years it is only expected to be close to the European average. Reforms that strengthen labour supply, together with a sustainable pension system, help mitigate the negative economic effects of ageing.

Population ageing is a global megatrend—one that affects everyone and everything. Japan was the first modern country to experience rapid ageing, and its sluggish growth has been closely monitored since the 1990s. Following Japan, the second-fastest ageing advanced economy has been Finland, where the old-age dependency ratio began to rise sharply around 2010.1 The number of elderly people increased by roughly 430,000 between 2010 and 2024, a dramatic shift for a small country. According to Statistics Finland, the number of employed persons grew by only about 100,000 over the same period—an average of 0.3 per cent per year.

Since slow growth in the number of employed people signals weak economic expansion, stronger productivity growth would be required to lift GDP growth. Yet productivity growth in Finland has remained modest. The slow increase in the wages and salaries sum has resulted in subdued tax revenue growth and mounting pressures on public finances. As a result, Finland’s public sector has accumulated substantial debt over the past 15 years.

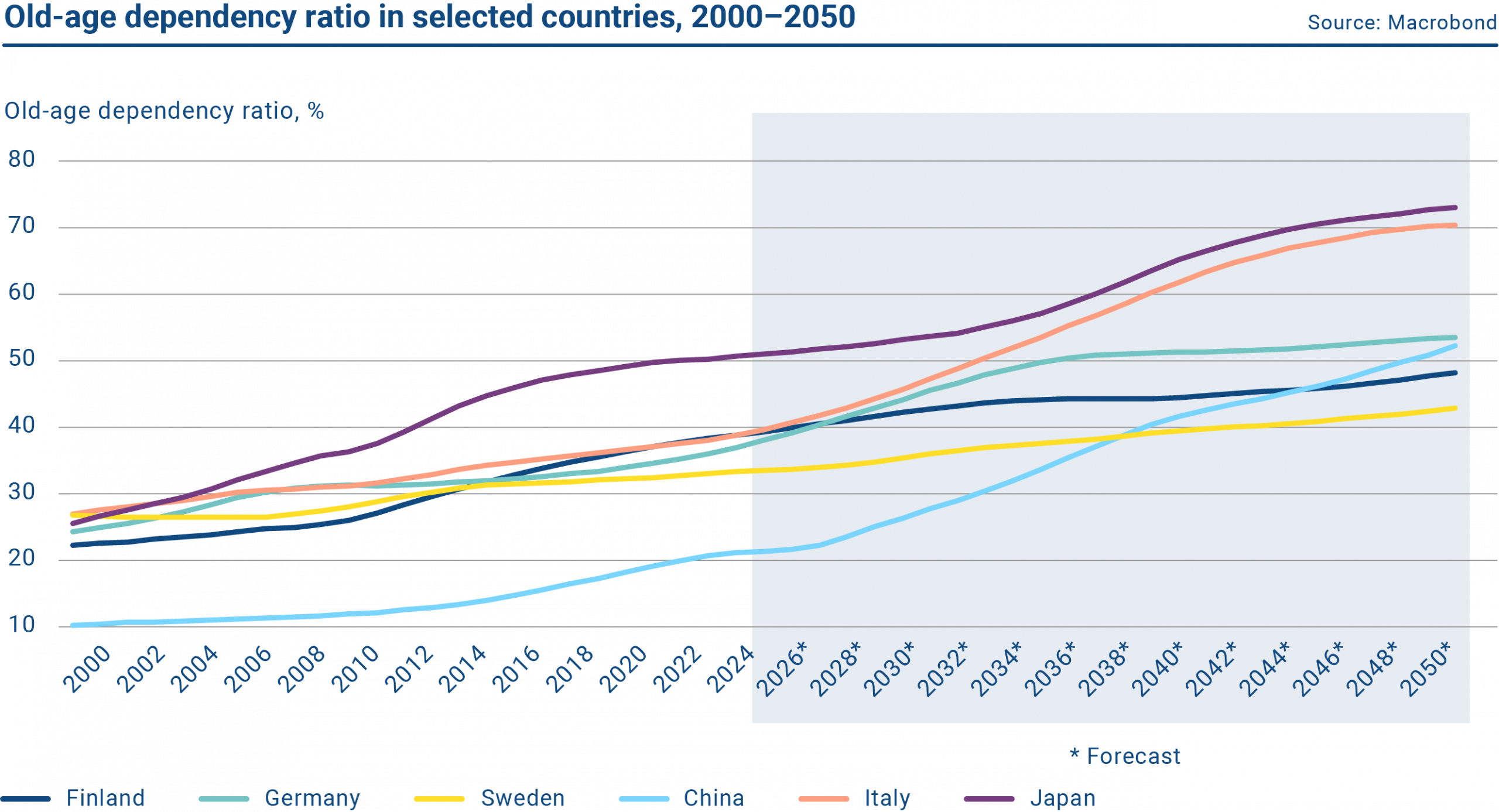

The graph shows the old-age dependency ratios in selected countries 2000-2050.

The conclusion is clear: the 2010s were an exceptionally challenging decade for Finland from a demographic perspective, and this was reflected in both economic growth and public finances. At the same time—and this is a key message for Finland’s economic outlook—the most intense phase of demographic adjustment is now largely behind us.

How population ageing affects economic growth

Macroeconomic research provides strong evidence that demographic shifts are closely linked to both economic and productivity growth.2

Slow growth—or even contraction—in labour input dampens an economy’s potential growth. Labour is a fundamental factor of production: the more pair of hands at work, the higher the level of output. In Finland, the working age population declined between 2010 and 2024, although the number of employed persons increased slightly. This reflects the economy’s inherent ability to adapt to an ageing population. Even so, it is clear that both economic activity and employment would likely have grown faster had the working age population expanded rather than contracted.

A larger elderly population also drives higher public expenditure. The immediate impact comes through rising pension costs, but over time public spending on healthcare and elderly care also increases. If these expenditures grow unchecked, the outcome is higher taxation, cuts in public services, or more public debt—or some combination of the three.

Ageing also raises the average age of the working‑age population. Beyond a certain point, age correlates negatively with individual productivity. Naturally, there is substantial individual variation here as not all people experience decline in productivity before retirement age. At the population level, however, the effect is clear: demographic ageing tends to slow productivity growth across the economy.

Ageing is further associated with shifts in individual preferences, particularly regarding risk‑taking. Risk appetite typically declines with age. This manifests in several ways: firms may become more cautious to invest and expand, individuals may be less willing to take on debt, and workers may be less inclined to change jobs. All of these factors play a central role in shaping long‑term economic growth.

Finland’s situation is improving

Kotamäki and Lehtimäki (2025) estimate that Finland’s standard of living, productivity and debt ratio would be broadly comparable to Sweden’s today had the country not gone through the intense ageing phase of the 2010s.

Population ageing has exacerbated Finland’s economic challenges, but there are signs of improvement ahead. According to demographic projections, the most intensive phase of Finland’s structural shift is now largely behind us, and the coming years are expected to bring a somewhat milder ageing trend. This fundamentally reshapes Finland’s growth prospects. The 2030s offer structurally stronger conditions for growth than the 2010s, as the negative leverage effect of ageing weakens and the positive impact of labour‑supply‑enhancing reforms strengthens.

It is entirely possible that, supported by reforms that boost labour supply, Finland could move onto a higher growth trajectory in the coming years as demographic ageing slows. Measures that increase labour supply have been—and will continue to be—crucial, as the economic effects of ageing can be mitigated by increasing the number of employed people. A clear example is the 2017 pension reform, which raised the statutory retirement age and linked it to life expectancy. In addition, labour‑based immigration can help alleviate labour shortages.

The rest of the world Is turning grey

Finland and Japan have been at the forefront of rapid demographic ageing. Countries such as Italy, Greece and Portugal have also aged, but over a much longer period.

The global landscape is set to change dramatically as an increasing number of countries enter a phase of rapid ageing. A striking example is China, where the roughly one‑billion‑strong working‑age population is projected to shrink by about one quarter over the next 25 years.

There are, however, countries where ageing has progressed much more slowly. Sweden, Denmark and the United States are examples of economies where the population is indeed ageing, but at a markedly different pace compared with many other Western nations.

Finland’s relative position improves as demographic pressures become lighter here than in many peer countries.

These developments have several implications. First, Finland’s relative position improves as demographic pressures become lighter here than in many peer countries. Today, Finland is among the most aged countries in the EU when measured by the old‑age dependency ratio; in 25 years, Finland is expected to be close to the EU average—implying significantly faster ageing elsewhere in Europe. Second, the global ageing trend may reshape the international economic landscape, as a growing number of countries confront the financial challenges associated with a rapidly ageing population.

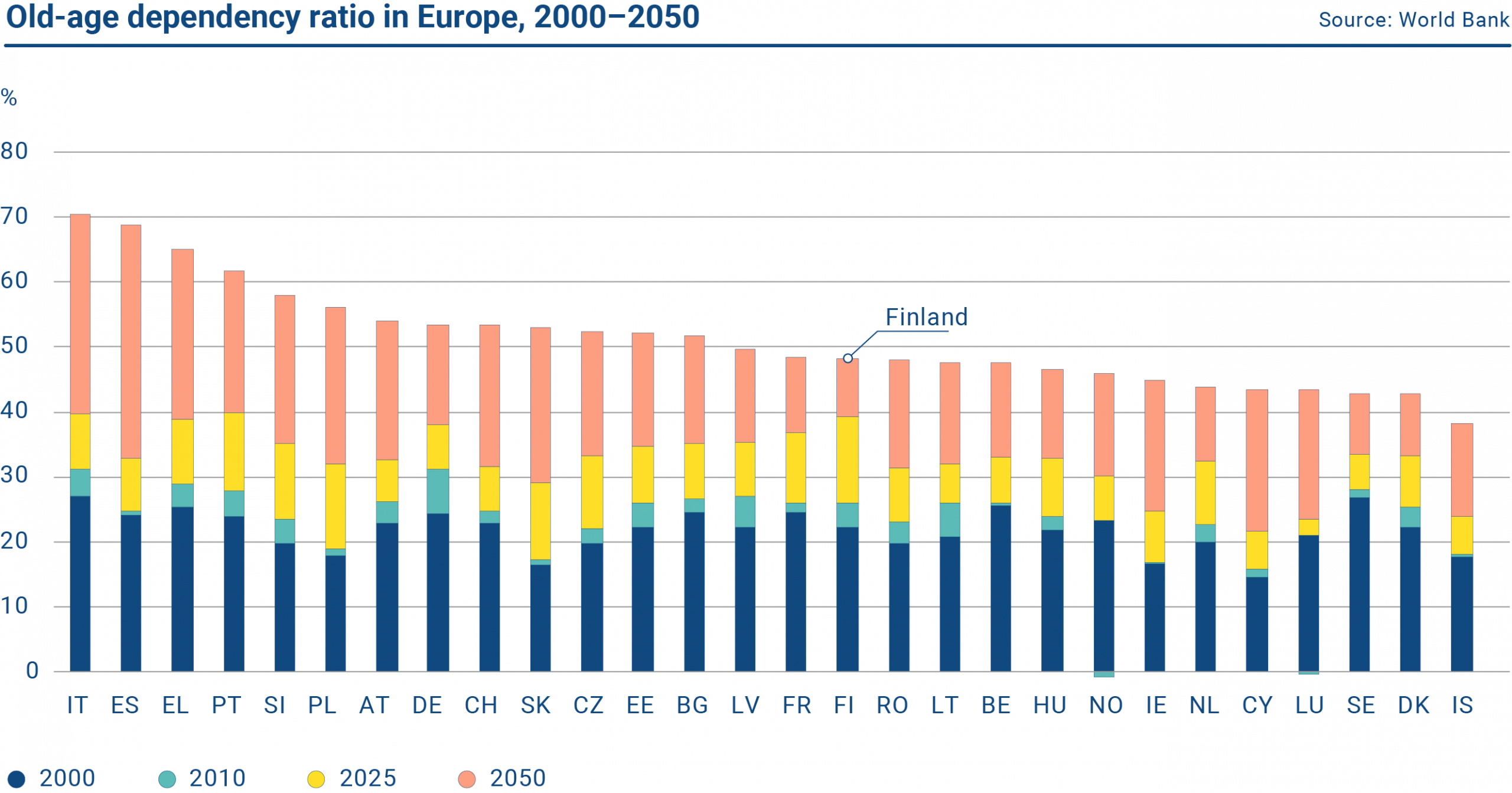

The graph shows the old-age dependency ratios in Europe 2000-2050.

Finland’s most rapid phase of demographic ageing is now behind us, creating the conditions for stronger economic growth than in the past decade. While Finland’s population will continue to age, the challenge ahead is of a different magnitude than what the country has already experienced—or what many of its peers are now facing.

Pension system as a lever for public finances

The pension system is a central component of Finland’s public finances. Despite the need for future reforms, the latest long‑term assessments indicate that the system is sustainable and does not face immediate pressure for contribution increases. Pension contributions are high, but they are matched by comprehensive pension benefits.

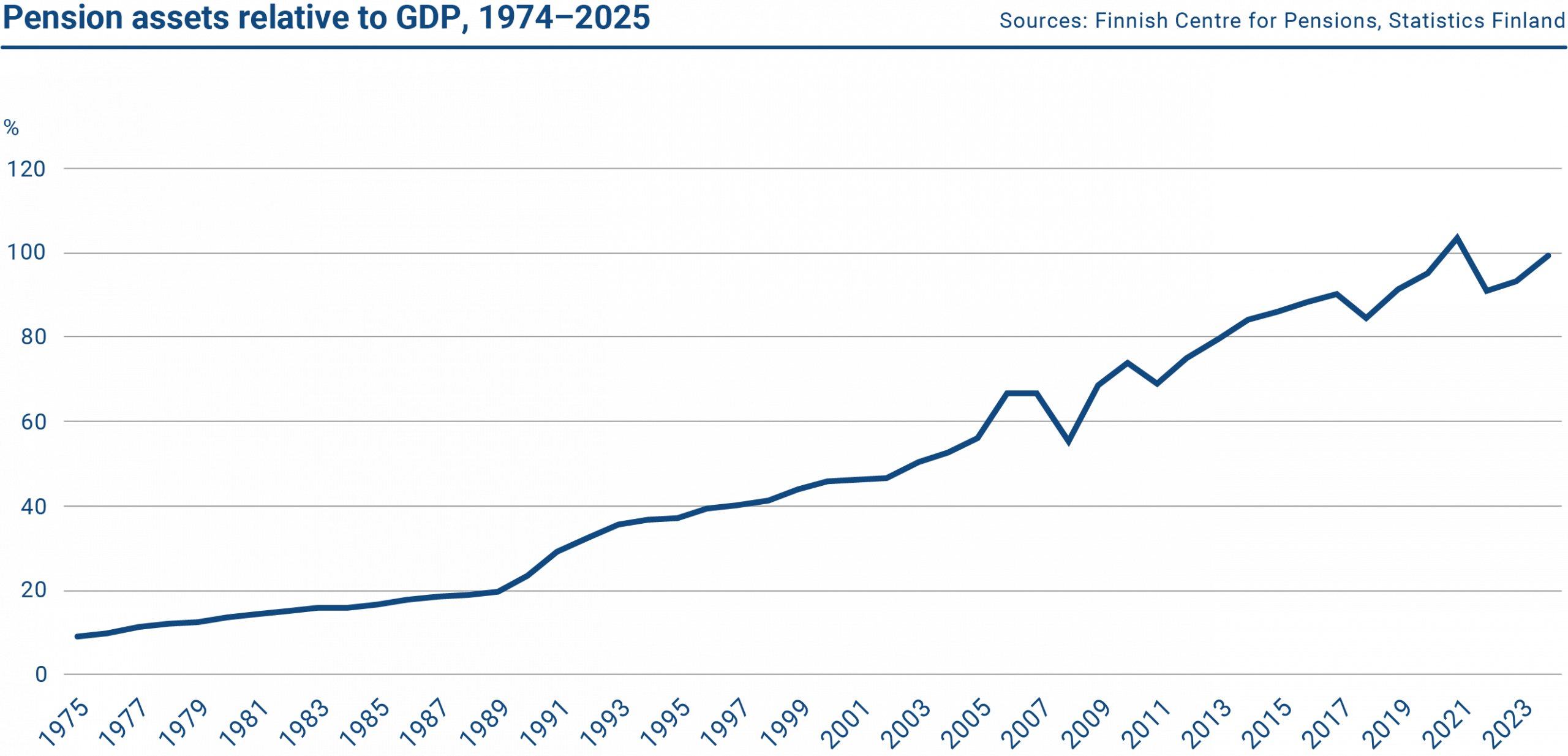

Finland is an exception among advanced economies: roughly EUR 285 billion in pension assets has been accumulated. In many countries, prefunding is limited, meaning that ageing translates more directly into higher taxes, higher insurance contributions or increased public debt. According to Statistics Finland’s 2022 estimate, Finland’s total pension liability amounts to roughly EUR 900 billion, reflecting the system’s long‑term commitments. The accumulated funds help finance future pensions.

Finland’s earnings‑related pension funds have improved the efficiency of pension financing through the financial markets. Contributions have been invested with a long‑term horizon in higher‑risk assets, generating returns that have exceeded the central government’s funding costs (the nominal return of pension insurers between 1998 and 2024 averaged around 5.7%). This return differential reflects the longer investment horizon and greater risk‑bearing capacity of pension funds, and has helped spread the fiscal burden of ageing over time.

In this sense, the pension system has successfully leveraged pension contributions through financial markets. The trade‑off has been higher pension contributions in the short term.

Most Finnish pension assets are invested abroad, meaning that partial funding does not fully translate into a larger domestic capital stock. What matters, however, is the income stream: foreign investment returns finance part of future pensions and provide a buffer if domestic wages and salaries sum growth falls short of expectations. Without partial funding, the adjustment would fall more directly on taxes, contributions or debt—measures that would more readily weaken labour supply and investment.

The recently agreed investment reform, which increases the equity share in pension portfolios, is expected to grow pension assets over time, provided that long‑term equity market performance remains favourable.

Partial funding and investment returns reduce the expenditure pressures associated with ageing, but they also shift the timing and distribution of the adjustment. The need for abrupt tightening diminishes, supporting more stable conditions for economic growth.

Diagrammet visar utvecklingen av Finlands pensionstillgångar i förhållande till BNP åren 1975–2024.

Conclusion: Finland’s next growth chapter may be more favourable

Finland’s most rapid phase of demographic ageing is over. This single fact will reshape the country’s economic dynamics over the coming decades more than any individual policy measure.

Growth barriers still exist, but they are no longer reinforced by demographic headwinds to the same extent as before.

Looking ahead, Finland’s sources of growth will be labour‑supply expansion, productivity gains and faster adoption of new technologies, alongside increased investment, stronger skills and proactive fiscal stabilisation.

Finland’s population will continue to age, but the pressure is easing—just as the rest of the world begins to grey at a faster pace. This shift gives Finland better growth conditions than it has had for quite some time.

1 The old-age dependency ratio is the proportion of the elderly population relative to the working‑age population

2 See e.g. Aiyar et al. (2016), Maestas et al. (2023), or Kotamäki and Lehtimäki (2025).